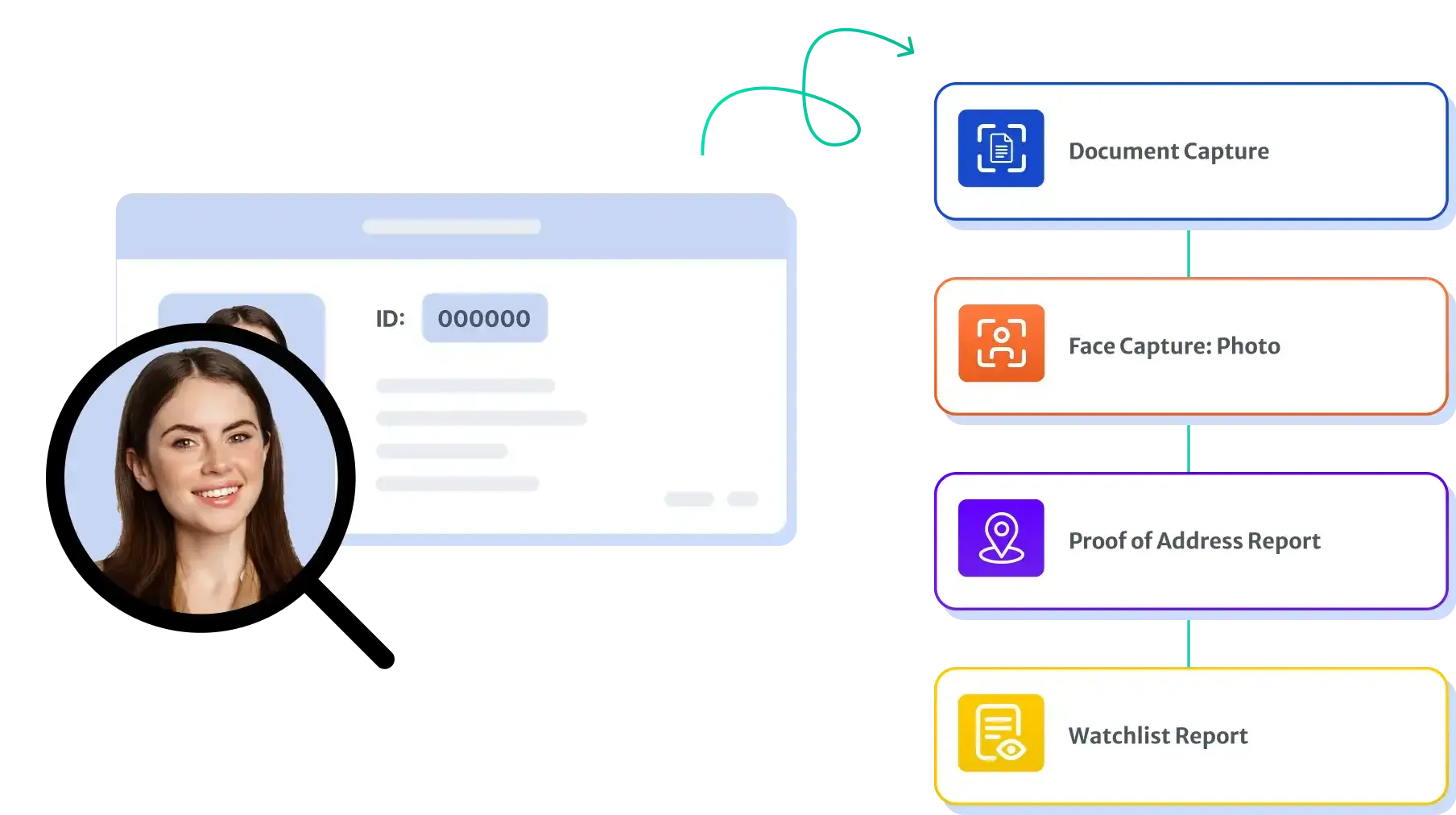

Superior Customer Due Diligence Processes

Automated continuous screening and monitoring solution that leverages ML and data analytics to ensure exhaustive document forensics, CDD, and AML checks while providing seamless customer experiences

Industries That Can Leverage A Fraud Prevention Solution

Banking

Onboard retail and corporate customers with full AML, KYC and case management.

Insurance

Onboard policyholders and brokers with KYC, KYB and sanctions screening in one flow.

Trade Finance

Verify counterparties, beneficial owners and trade documents before issuing any instrument.

Gaming & Gambling

Cut player drop-offs while staying compliant with strict KYC and responsible-gaming rules.

Fintech

Launch compliant products faster with a modular KYC, KYB and AML stack.

Lending

Underwrite faster with end-to-end KYC, income checks and risk scoring built in.

Payments

Verify senders and beneficiaries in milliseconds before clearing any transaction.

Crypto

Stay travel-rule compliant and screen wallets in real time across global watchlists.

Fraud Prevention Challenges

Modern fraud is faster, more automated and more cross-channel than ever — yet most stacks were built for one rail and one fraud vector.

Why Companies Need Fraud Prevention Solution

Stop Identity Fraud

Block synthetic identities and stolen credentials at the door with strong IDV.

Detect Transaction Fraud

Catch unusual patterns in real time across every payment rail.

Reduce Chargebacks & Losses

Cut financial loss from fraud by routing only the truly risky cases to manual review.

Protect Customer Experience

Approve good customers instantly and reserve friction for the genuinely risky.

Stay Ahead of New Attack Vectors

Detect deepfakes, mule networks and account takeover with continuously updated models.

Audit-Ready Investigations

Capture every signal and decision so investigators and examiners see the full story.

Why Companies Rely On KYC Hub For Fraud Prevention

Stop fraud across identity, transactions and account behaviour — on one platform built for modern attack vectors.

Superior Fraud Pattern Detection

Combine entity resolution, graph analytics and AI to catch patterns rules-only systems miss.

Improved Customer Experience & Compliance

Approve good customers in seconds while routing only edge cases to manual review.

Reduced Latency & Improved Performance

Score every transaction in milliseconds without slowing the payment flow.

Detecting Identity Frauds

Block synthetic identities, replay attacks and deepfakes with frame-level liveness.

[ RELATED ]

KYC Hub Products & Solutions That Can Help With Fraud Prevention

Discover more about our products and solutions. Explore the rest of the KYC Hub stack.

Any questions? We got you.

Discover more about our products and solutions. Embark on your journey towards seamless compliance.