Identity Verification for Neobanks: How It Works and How to Choose a Provider

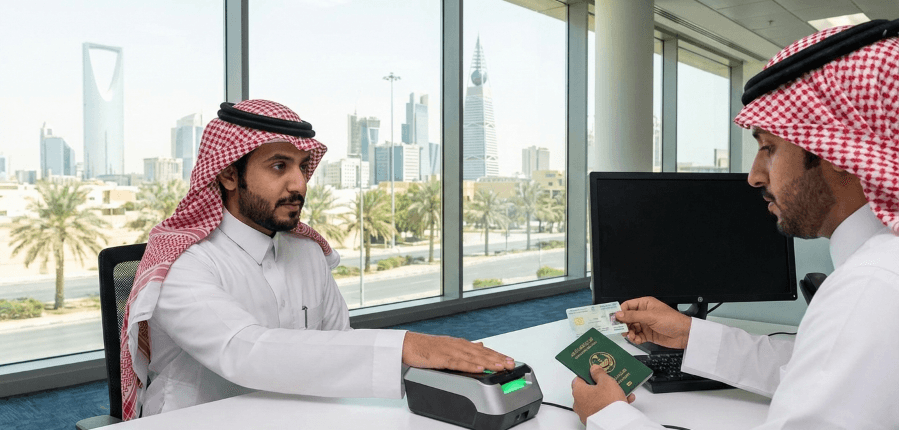

Identity verification for neobanks is how a digital-only bank confirms a new customer is a real person, who they claim to be, before an account ever opens. No branch. No in-person check. Everything happens remotely, in seconds, drawn from a document photo, a selfie, and a set of background checks that run behind the scenes. At a neobank this sits right at the front door of onboarding, and it pulls double duty there: stopping fraud while satisfying Know Your Customer rules.

What lurks behind that front door changed shape over the past year. Fully remote onboarding has become the norm, which means attackers can now feed AI-generated faces and forged documents straight into the flow. Deepfake selfie attempts rose 58% in 2025. Injection attacks, where manipulated video bypasses the camera and gets pushed directly into a verification system, slid from a fringe technique into a common one over the same stretch. Onboarding speed still wins customers, but that speed only holds up when the verification sitting underneath it is strong.

Neobanks are the digital-first pioneers of modern banking. Customer convenience comes first, and technology does the heavy lifting to deliver financial services that are fast, accessible, and tailored to the individual. Since everything runs online, they lean on remote verification to confirm who their customers are and to keep fraud out. What follows walks through what identity verification for neobanks actually involves: how the flow works, the rules that shape it in 2026, and how to weigh one provider against another.

What Is Identity Verification (IDV)?

Identity verification confirms that an individual is who they claim to be. It tests the authenticity of the personal information a person submits, usually against a government-issued document such as a passport or driver's license, and then ties that document back to the living person presenting it.

At a neobank, this check fires at account registration and again whenever risk spikes later on. Compliance begins here too. Get verification right and you keep fraudsters out while staying inside the rules. Get it wrong and you eat both the loss and the regulatory exposure.

How Identity Verification Works for Neobanks

Most neobank verification flows follow the same shape, even when the underlying technology differs by vendor. A customer submits an identity claim. The system tests it. Back comes a decision, almost always with no human in the loop.

In practice that breaks into a few steps:

- Capture. The customer photographs a government ID and then takes a selfie inside the app. Capture quality matters more than people expect, because blurry inputs drive rejections that have nothing to do with fraud.

- Document validation. Here OCR reads the document, the system checks it for tampering, forgery, and expiry, and the extracted data gets matched against trusted sources wherever they exist.

- Biometric match and liveness. The selfie is compared to the face on the document, and a liveness check confirms a real, present person rather than a photo, a mask, or a replayed video.

- Screening. Now the verified identity runs against sanctions lists, politically exposed person lists, and adverse media before the account is allowed to open.

- Decision and record. The system returns approve, decline, or refer for review, then writes an auditable record of how it reached that answer.

A good neobank flow handles the common case end to end and escalates only the edge cases. One distinction does the work here: it separates a verification process that scales from one that buries a small compliance team in manual review.

The Role of Identity Verification in Neobanking

Once you understand what IDV is, the reason it matters to neobanks comes into focus. Strong verification protects customer information, builds trust, and keeps financial transactions sound in an entirely digital setting. A few benefits stand out.

- Native to a digital platform. A remote verification method fits the existing infrastructure of a purely digital bank. Configurable security layers then let a neobank add checks where risk runs higher, hardening the process without rebuilding it.

- A flow you can configure. When verification adapts to product, geography, or risk segment, a neobank can tune the experience per customer instead of forcing everyone down the strictest path.

- Faster onboarding. Remote verification clears a new customer in seconds rather than days. People abandon a signup the moment it drags, so in that market the speed is the product.

- Insight from every check. Data comes out of each verification, and a neobank can analyze it to sharpen risk decisions over time.

- Global reach. One flow verifies customers across many countries, so a neobank can onboard worldwide without standing up a separate process for each market.

- A barrier against identity fraud. Confirming that an identity is genuine keeps impostors and synthetic identities out, and technology that catches forged documents drops the risk from fake IDs in particular.

- Audit trails and reporting. Every check leaves a record. Hand that documentation to a regulator and it proves the controls work, and it doubles as a source of insight for ongoing improvement.

The Threats Reshaping Neobank Verification in 2026

Verification deserves fresh attention because the attack surface widened fast. Three pressures now define the problem for neobanks.

First, the deepfake. Tools that generate a convincing face, or swap one in real time, are cheap and easy to find. Deepfake selfie attempts climbed 58% in 2025, and roughly one in five biometric fraud attempts now involves a deepfake. A static selfie check, standing alone, no longer holds.

Second, the injection attack. Rather than hold a fake up to the camera, an attacker feeds manipulated images or video straight into the verification pipeline and skips live capture altogether. Catching it means reading device and metadata signals, not only the visible image.

Third, synthetic identity fraud. A fraudster stitches together real and fabricated details to build an identity that has never existed, then opens an account with it. Neobanks make a favored target precisely because onboarding is remote, and weak verification waves these fake identities through. Strong liveness detection and document authentication exist to stop exactly this.

Challenges Neobanks Face in Identity Verification

Industry-wide threats sit on top of a second set of challenges, ones that come baked into the neobank model itself. Working through them is how a neobank earns a reputation for trustworthiness.

- Reputation and history. Past links to money laundering have drawn scrutiny to neobanks. Sustained vigilance and tighter regulation are rewriting that story now, bringing more accountability and a clearer commitment to compliance.

- Remote onboarding. No face-to-face contact makes identity theft and account takeover harder to spot. Proving an identity is genuine through a screen alone demands strong verification mechanics.

- Thin customer data. Traditional banks hold years of interaction history. A neobank often starts with little more than a name, an address, and a date of birth, which makes early suspicious behavior tough to catch.

- A global customer base. Operating across borders throws a neobank into a patchwork of AML and KYC regulations. Document verification requirements and scrutiny levels shift from one jurisdiction to the next, and that variety piles on real complexity.

- Security versus privacy. A neobank has to verify rigorously while respecting how much data customers are willing to hand over. Collecting only what is needed, then protecting it well, is what builds trust with people who are wary of how their information gets used.

Identity Verification as a Service for Neobanks

Most neobanks do not build verification in-house. They consume it as a service instead, calling an external provider over an API at the moment a customer signs up. One request sends the document and selfie out; one response comes back carrying a risk decision. People call this identity verification as a service, and it has become the default model for digital banking because it removes the need to maintain document libraries, biometric models, and watchlist feeds yourself.

An API approach is not the risk some assume it to be. What actually matters is the provider behind it: how it handles data, where that data lives, which certifications it holds. Recognized controls such as ISO 27001 and SOC 2 Type II signal a provider doing the heavy compliance lifting on your behalf. Architecture turns into a liability only when the operator running it cuts corners on data handling.

This model also folds KYC identity verification and screening into one step. A single call confirms the document, matches the face, and runs sanctions, PEP, and adverse media checks, so a neobank meets its onboarding obligations in one pass rather than bolting separate tools together.

Ongoing Verification and Perpetual KYC

Verification at signup is no longer the end of the job. A neobank has to keep checking after the account opens, because a customer's risk can change long after day one, and regulators expect exactly that.

Sanctions, PEP, and adverse media lists move constantly, so a one-time screen at onboarding goes stale fast. Perpetual KYC swaps fixed annual reviews for event-driven ones: a re-screen or a re-verification fires when something in the customer's profile or behavior changes, not on a calendar. Biometric re-verification can also step in at higher-risk moments, asking a customer to confirm a real, live face before a sensitive action goes through. Assurance stays high that way, and nobody gets dragged through friction they do not need.

When you weigh providers, look hard at how each one handles this continuous layer. Verify only at the front door and you leave a gap that opens the day after onboarding.

How to Choose the Right IDV Solution for Neobanks

With these pressures in mind, picking the right identity verification solution becomes one of the more consequential calls a neobank makes. Landing on a fit takes careful evaluation paired with real testing against your own traffic. A few factors carry the most weight.

1. Accuracy. Look for technology that verifies precisely across a diverse population. It should authenticate many document types, from passports to driver's licenses, and match faces reliably across different ethnicities, genders, and backgrounds. Uneven accuracy is both a fraud gap and a fairness problem.

2. Compliance. Whatever regulations apply to you, the solution has to meet them and keep current as they shift. Collecting and verifying the right customer details falls under this, plus adapting when rules change, so your controls never fall behind supervisory expectations.

3. Fraud defense. Given the 2026 threat picture, liveness detection and anti-spoofing are non-negotiable. A capable solution resists deepfakes, presentation attacks, and injection attacks rather than checking a face in isolation.

4. User experience. Customers should find the flow simple, and onboarding should never get harder than it needs to be. Clean interface, clear instructions, quick turnaround: those count for as much as accuracy. Backing for multiple languages, and for customers with disabilities, widens who you can serve.

5. Scalability. Pick something that grows with you. Rising onboarding volume, new technology and rules, expansion into fresh markets, all of it should land without a rebuild.

6. Reputation and security. Favor a vendor with a real track record, a serious customer base, and a clear focus on data security. Worth as much as the technology itself: a strong technical team that helps you implement and maintain the solution.

Whichever way you lean, test the shortlist against your own onboarding traffic before you commit. Demos on clean sample data rarely predict how a tool behaves against live fraud. See how KYC Hub's identity verification handles your onboarding flow.

How KYC Hub Supports Neobanks

KYC Hub's identity verification is built for global customers and the exact pressures above. Facial biometrics and liveness sit at the center. Eye movement gets tracked, and texture and surface analysis runs alongside it. Video detection separates a live person from a clip or a photograph, and the anti-spoofing layer is built to catch tampering and deepfakes.

Onboarding is designed to finish in seconds. Auto-fill speeds the form along, checks run in parallel, and the journey adapts to risk so legitimate customers never get slowed down. Configure every step of the flow per product, geography, or risk segment without writing code, and run it across web, mobile, in-branch, or API. Every check writes to a tamper-evident audit log, which keeps reporting and compliance clean the moment an examiner asks how a decision was made. For high-risk transactions, risk-based re-verification adds a layer of assurance after onboarding rather than only at the front door.

Bring those pieces together and a neobank can verify customers worldwide, keep fraud out, and stay audit-ready without sacrificing the fast onboarding its customers expect. Book an identity verification demo to see it run against your own use case.