KYC vs eKYC: Which Method Should Your Institution Use in 2026?

Twenty-seven billion. That’s how many Aadhaar authentication transactions ran through India’s identity infrastructure in FY 2024–25, a number UIDAI confirmed in April. For any regulated entity still debating which verification method to standardize on, that figure puts the entire KYC vs eKYC conversation in perspective.

Banks still processing paper-based checks are spending around 18 minutes per customer on something that digital KYC can finish in under 30 seconds. Same regulatory outcome. Very different cost structures underneath.

The going-digital debate is effectively over. Eighty-five percent of financial product onboarding now runs through electronic KYC, a share that climbed six points in a single year. The KYC vs eKYC conversation has shifted to something more granular: which digital method works for which product? Aadhaar OTP KYC, V-CIP, and in-person verification are not variations of the same thing. They carry different regulatory ceilings, different fraud exposure levels, and very different costs per customer. Most compliance teams have not drawn those lines clearly enough.

KYC vs eKYC vs Video KYC: Why the Three Methods Are Not Interchangeable

The RBI revised the rules twice in 2025, and both rounds had real consequences for institutions still trying to finalize their KYC vs eKYC strategy.

The June amendments gave some breathing room on periodic re-verification, pushing deadlines for low-risk individuals to June 30, 2026. Rather than freezing accounts mid-cycle, transactions could continue under monitoring while institutions worked through their backlogs. For anyone sitting on thousands of pending re-verifications, that extension was worth something.

The August directions were a bigger shift in the KYC vs eKYC regulatory landscape. Aadhaar Face Authentication was formally recognized as a valid identification method, and the definition of acceptable digital KYC was widened. January 1, 2026 was set as the date by which IT systems, Banking Correspondent workflows, and internal documentation all needed to reflect those changes. That date has come and gone. Institutions that did not make the transition are now working under scrutiny rather than ahead of it.

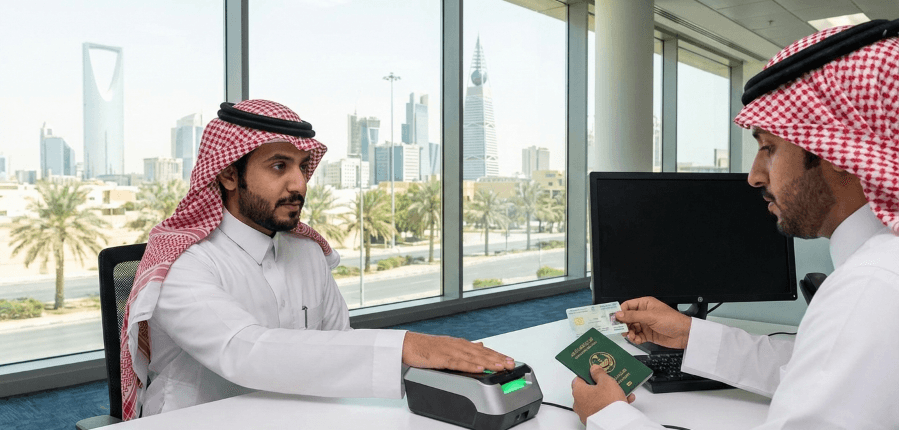

In-person KYC has been around the longest and carries the fewest regulatory restrictions. A customer presents original documents at a branch, an authorized officer checks them face-to-face, and the verification is done. It is the slowest and most expensive option by a significant margin, but it remains the default for high-net-worth onboarding and complex entity structures where regulators want the highest level of diligence.

Aadhaar OTP KYC, the most commonly discussed form of eKYC in India, works very differently. The customer provides their Aadhaar number, a one-time password arrives on their registered mobile, and the system pulls verified demographic data and a photograph directly from UIDAI. The entire process takes seconds. No documents to submit, no branch to visit, no appointment to schedule. The trade-off is a regulatory ceiling that limits it to lower-risk products with transaction caps, something institutions often underestimate when they first start designing their onboarding flows.

V-CIP sits between the two in the KYC vs eKYC vs video KYC spectrum. An authorized officer conducts a live, recorded video call with the customer, verifies documents on camera, captures geo-tagged footage with timestamps, and runs a face match against UIDAI records. The session is encrypted end-to-end with liveness detection built in. It delivers full KYC status with no transaction limits, and the 2025 amendments expanded its scope to cover both onboarding and periodic updates, which is where the eKYC vs video KYC decision becomes operational for institutions running mixed product portfolios.

KYC vs eKYC: Four Variables That Actually Drive the Decision for Banks and NBFCs

When choosing which method to deploy, four variables matter more than anything else: regulatory ceiling, fraud resistance, customer drop-off, and cost per verification. Understanding how KYC vs eKYC performs across each of these is what separates a well-designed onboarding strategy from one that creates problems at scale.

Regulatory ceiling is the place to start, and it is non-negotiable.

Aadhaar OTP KYC cannot open a full-KYC savings account. That single limitation means any institution offering loans, credit cards, or investment products needs either V-CIP or in-person verification. RBI has shown no inclination to relax this boundary, and building a product strategy that ignores it creates compliance exposure that compounds quietly over time.

Fraud resistance in the KYC vs eKYC comparison does not break the way most people expect.

In-person verification catches basic document forgery reasonably well, but it consistently misses more sophisticated manipulation that AI-driven video KYC systems can flag quickly. V-CIP adds encrypted video evidence, automated face matching, and geo-tagging that identifies location spoofing patterns that branch officers have historically missed. OTP-based eKYC is the weakest on this dimension. It confirms that the Aadhaar holder received a code on their registered phone. Nothing beyond that.

Drop-off rates flip that ranking, and this is where institutions often get caught off guard.

In-person KYC loses a meaningful share of customers before they ever complete the process. OTP-based eKYC flows see the lowest abandonment, typically taking under two minutes with no camera required and very little friction. V-CIP sits in the middle, with drop-offs tied to camera permissions, bandwidth issues, and some customer hesitation around live video interactions. Understanding your customer base is just as important as understanding the regulatory framework when making this call.

Cost per verification is where the KYC vs eKYC differences become impossible to ignore at scale.

In-person KYC runs roughly Rs. 150 to 300 per customer. Aadhaar OTP eKYC costs Rs. 5 to 15. Video KYC for banks and NBFCs typically falls between Rs. 40 and 80 depending on infrastructure and volume. When onboarding runs into the thousands of customers a month, those differences stop being marginal and start shaping the unit economics of the entire operation.

What the Numbers Show About eKYC Adoption in India

India’s e-KYC market was valued at $26.3 million in 2024, and projections put it at $139.3 million by 2033, growing at over 20% annually. Cumulative Aadhaar eKYC transactions crossed 23.9 billion by April 2025, growing nearly 40% year-over-year according to UIDAI data. Face authentication alone crossed one billion transactions in a single year.

Infrastructure operating at that scale does not plateau. It builds on itself, and the institutions that built their systems early are already operating at a structural advantage compared to those still working through the transition.

KYC vs eKYC: Matching the Right Method to the Right Risk Level

Running every customer through the same KYC flow regardless of product type or risk profile is one of the more common and costly mistakes institutions make. It leads to overspending on low-risk accounts while under-verifying high-value ones, creating inefficiency at both ends without improving compliance in either direction.

The institutions getting the KYC vs eKYC question right are layering all three methods based on where each one genuinely fits.

Aadhaar OTP KYC handles low-risk, high-volume onboarding efficiently and at low cost. Video KYC through V-CIP covers full-KYC remote verification without requiring a branch visit. In-person KYC stays reserved for high-risk cases or complex entity structures where regulators expect the highest standard of diligence.

That is the model RBI’s current framework supports, and the one it increasingly expects institutions to be running.

How KYC Hub Helps Institutions Operationalize KYC vs eKYC at Scale

The challenge most institutions face is not figuring out which method to use in theory. It is running all three in practice without creating separate compliance workflows, ballooning costs, or friction in the customer journey.

Rather than treating Aadhaar OTP KYC, V-CIP, and in-person verification as three separate workflows maintained independently, KYC Hub enables institutions to orchestrate all three within a single platform. Customers are routed dynamically based on product type, risk level, and regulatory requirements without manual intervention at each decision point.

For Video KYC specifically, KYC Hub provides a fully compliant infrastructure that includes AI-powered liveness detection, real-time document verification, face matching against ID records, and geo-tagging with audit-ready video logs. Banks and NBFCs can meet RBI’s video KYC guidelines without needing to build or maintain the underlying infrastructure themselves.

Because the platform connects directly with onboarding, AML, and transaction monitoring systems, KYC stops being a fragmented compliance task handled in isolation and becomes part of a unified operational workflow.

Where the KYC vs eKYC Debate Stands Heading Into 2026

The KYC vs eKYC debate has moved well past the question of which method is better in the abstract.

The practical question now is whether institutions have built a system that uses each method where it genuinely fits, rather than where it is easiest to apply or cheapest to default to.

The January 2026 deadline has already passed. Institutions that moved early have already built layered, risk-based digital KYC verification into their onboarding processes and are operating with the cost and compliance benefits that follow. Others are working to close the gaps that built up while the debate was still theoretical, rethinking how onboarding should actually function at the scale they are now operating at.

The question is no longer what to adopt. It is how well, and how completely, you have already put it in place.

Aadhaar onboarding works until OTP delivery fails or a customer needs re-KYC. KYC Hub's India KYC platform covers those fallbacks, V-CIP included, without a second vendor. See a demo.