eKYC Explained: How Electronic Know Your Customer Works

eKYC, or electronic Know Your Customer, verifies a customer's identity remotely instead of in person with paper documents. It captures and validates identification documents and personal data electronically, then checks that data against trusted sources to confirm the customer is who they claim to be. For regulated businesses, the payoff is real: the same regulatory assurance as manual KYC, but onboarding that is faster, cheaper, and far easier to scale.

Most industries care about identity verification. Banks and financial institutions build their whole compliance posture on it. In most jurisdictions, customer identification systems are mandatory for these organizations, and as digital banking grew, identity verification got harder to do well at scale. eKYC is the answer that lets compliance teams keep pace with digital growth without giving up rigor.

How eKYC Works

Instead of an in-person document check, eKYC runs an electronic workflow the customer completes from a phone or computer. Most implementations move through three stages.

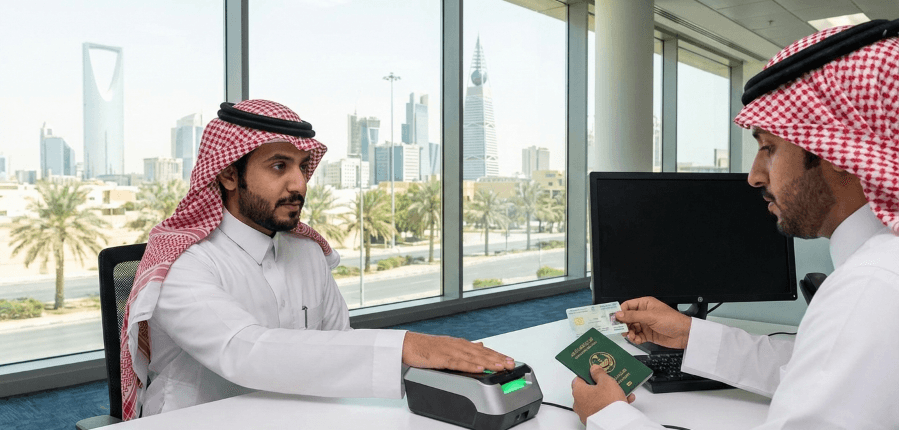

First comes identity capture. The customer presents proof of identity, usually by photographing a government-issued document such as a passport or driving licence. Optical character recognition reads the personal data off the document and fills in the application automatically, which cuts manual entry and the errors that come with it.

Next is biometric authentication. The customer submits a selfie or another biometric, and facial recognition matches it against the photo on the document they uploaded. Most users find this the easiest step, since the camera on any modern smartphone is already up to the job.

Last is a liveness check. Here the customer proves they are a real, present person rather than a static image or a replay attack. That might mean a short live video, a guided selfie, or a fingerprint scan on a supported device. Run end to end, the three stages give a compliance team a verified, auditable identity record without any face-to-face contact.

Types of eKYC

There are several eKYC methods, and most enterprise deployments combine more than one to balance assurance against customer friction.

- Document-based eKYC captures the document digitally and checks the data against government and issuing-authority records to validate state-issued IDs such as passports and national identity cards.

- Biometric eKYC ties the identity to a live person using features the customer's own device captures, like facial recognition or a fingerprint scan.

- Knowledge-based authentication asks the customer pre-set questions only they should be able to answer. On its own it is the weakest of the bunch, so teams usually run it as a supporting layer.

- Hybrid eKYC folds several methods into one workflow when you want broader, more configurable verification.

The right mix depends on your risk appetite, the regulations you operate under, and the assurance level your customer segment demands. A capable global KYC solution lets compliance teams orchestrate these methods in one configurable flow instead of stitching together point tools.

eKYC vs Traditional KYC

Traditional KYC and eKYC split on one thing: how personal information gets gathered, processed, and validated.

Traditional KYC runs on paper records and manual review. The customer usually has to show up in person at a branch or office with physical documents, and an employee then cross-checks the identity document against databases and watchlists by hand. All that face-to-face, manual work slows onboarding to a crawl, and customers can wait days or even weeks for a decision.

eKYC is fully digital. Customers scan and upload their documents from home, and automated checks validate them in near real time. Going digital strips out the costs tied to paper, physical infrastructure, and manual labor, so onboarding that once took days can finish in minutes. Same compliance outcome, far better operations.

eKYC for Regulated B2B Use Cases

eKYC is less a single product than a capability, one that different regulated sectors adapt to their own onboarding and risk obligations.

Banks and fintechs use it to open accounts remotely while meeting customer due diligence requirements, and because it sets a verified identity baseline at account opening, the same workflow feeds ongoing transaction monitoring. Payment firms and crypto businesses lean on eKYC to onboard at scale across jurisdictions while keeping false rejections low. Insurers and investment managers reach for it to verify policyholders and investors before any high-value relationship begins.

The buyer, in every one of these cases, is a compliance or operations team that needs verifiable, auditable identity assurance. It is not a consumer following a one-off how-to, and that is the lens this guide takes. Onboarding that spans multiple countries adds one more requirement: a provider that can adapt the verification flow to each jurisdiction's rules.

Benefits of eKYC for Compliance Teams

Adopting eKYC pays off in measurable ways for the business and a better experience for the customer.

Start with the customer experience. Cut out the branch visit and the manual paperwork, and onboarding shrinks to minutes. Completion rates climb and drop-off falls. Because verification is mobile-first, a customer can finish the whole thing on a device they already carry.

Then there is cost. Manual KYC piles on administrative overhead for storing, verifying, and handling documents. Automate those steps and that overhead drops, which frees compliance staff to chase genuine risk instead of routine data entry.

Last is security and control. Electronic workflows apply strong encryption, layered verification, and consistent checks against sanctions and watchlists. Compared with paper records that can be lost, altered, or stolen, that lowers the risk of identity theft and fraudulent onboarding.

What to Look for in an eKYC Provider

Picking a provider is a strategic call. The platform sits at the front door of every customer relationship, so evaluate candidates against a few practical criteria.

Regulatory coverage comes first. KYC and AML regulations vary by region, so the solution has to conform to the rules in each market you serve and keep up as those rules change. A provider with experience across multiple legal environments lifts a real burden off your team.

Weigh data minimization next. As data-protection rules keep tightening, collecting and retaining personal information gets harder. Favor a solution that stores only what it needs and does not hold selfies or surplus identity data longer than required.

Then there is configurability. A rigid, one-size-fits-all flow ages badly. Hybrid models that pair automated checks with human oversight where it counts give you a process that flexes as your risk profile and product mix shift. Finally, weigh the commercial model. Compare subscription and per-transaction pricing against your expected volumes and your short and long-term cost picture.

How KYC Hub Powers eKYC

KYC Hub offers a global KYC solution built for banks and fintechs that need fast, compliant onboarding across markets. The platform leads with the capabilities a modern eKYC program depends on. Video KYC, identity verification, ID verification, digital signature, liveness checks, and phone verification all run inside a single configurable workflow.

With that breadth, a compliance team can run document capture, biometric matching, and liveness in one flow, route higher-risk cases to human review, and apply jurisdiction-specific rules without rebuilding the process for every market. The result is verified, auditable identity at onboarding, with less manual effort and faster time to first transaction. To see how the platform fits your onboarding and compliance requirements, get a free demo.