What is Know Your Customer (KYC)?

Know Your Customer, or KYC is an essential process for financial institutions, helping them verify their customers’ identity and assess the risks associated with them. In this beginner’s guide, we’ll delve into the world of KYC, its components, its importance, and various KYC regulations and solutions.

Know Your Customer (KYC) is essential in preventing financial crimes. Global banks spend over $1.6 billion yearly on KYC compliance. According to the United Nations, money laundering costs up to $2 trillion every year. KYC identifies and verifies customers with the aim of combating fraud, terrorism financing, and tax evasion. In 2023, more than 95% of financial institutions reported delays due to incomplete KYC data, focusing on the growing need for effective digital KYC verification solutions.

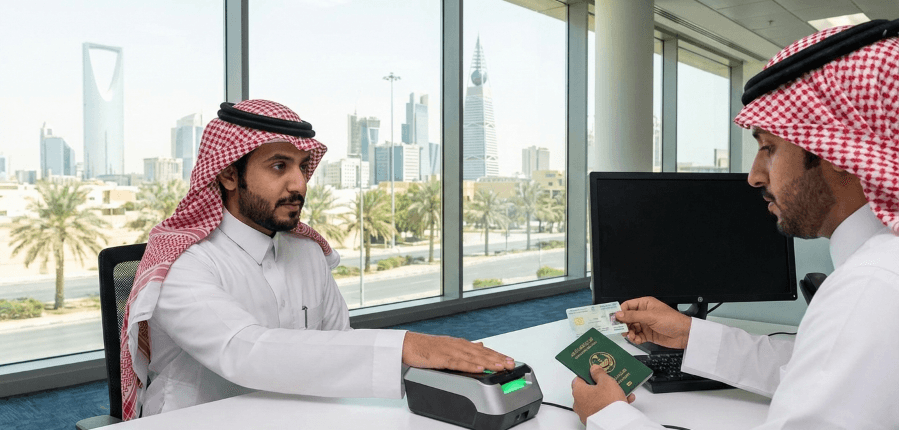

Financial crime is a serious issue that poses significant risks for businesses and individuals. As such, financial institutions need to have effective anti-money laundering (AML) procedures in place to prevent financial crime. One of the most crucial steps in AML compliance is KYC verification. KYC is a process that requires financial institutions to identify and verify the identities of their customers to ensure they are who they claim to be.

What is Know Your Customer (KYC)?

Know Your Customer (KYC) is the process used by financial institutions and other businesses to verify the identity of their customers and ensure they are who they claim to be. It involves collecting and verifying documents to prevent fraud, money laundering, and terrorist financing. The primary goal of KYC is to verify customers’ identities, ensure compliance with regulations, and reduce the risk of money laundering and terrorist financing.

The KYC process is essential to prevent financial fraud, money laundering, and other illegal activities. It involves collecting and analyzing various documents and data to determine customers’ identity, financial position, and risk profile.

What is the Full Form of KYC?

The full form of KYC is Know Your Customer.

Objectives of KYC

The main objective of KYC is to verify customer identities and prevent money laundering and financial fraud. The four primary objectives of KYC are:

- Customer identification,

- Risk management,

- Regulatory compliance, and

- Trust building to prevent financial crimes and ensure the economic system’s integrity.

Know Your Customer has been around for decades, but has gained increasing importance recently due to the growing risks associated with financial crimes. With globalization and digitalization, financial transactions have become more complex, making it easier for criminals to exploit vulnerabilities and carry out illegal activities.

This has led to the implementation of stricter Know Your Customer regulations by governments and financial authorities worldwide, ensuring that businesses take the necessary measures to protect themselves and their customers.

Implementing anti-money laundering (AML) measures is a crucial part of the KYC and AML framework, as they are vital tools for detecting and preventing illicit activities such as money laundering. AML policies within this framework typically include a set of procedures to monitor customers’ transactions, identify suspicious activity, and report such incidents to relevant authorities, thereby reinforcing the effectiveness of KYC procedures.

Overview of the KYC Process

The KYC process can be broken down into several steps, which include:

- Customer Onboarding: When a new customer seeks to establish a relationship with a financial institution, the institution must collect and verify the customer’s identification and other relevant information.

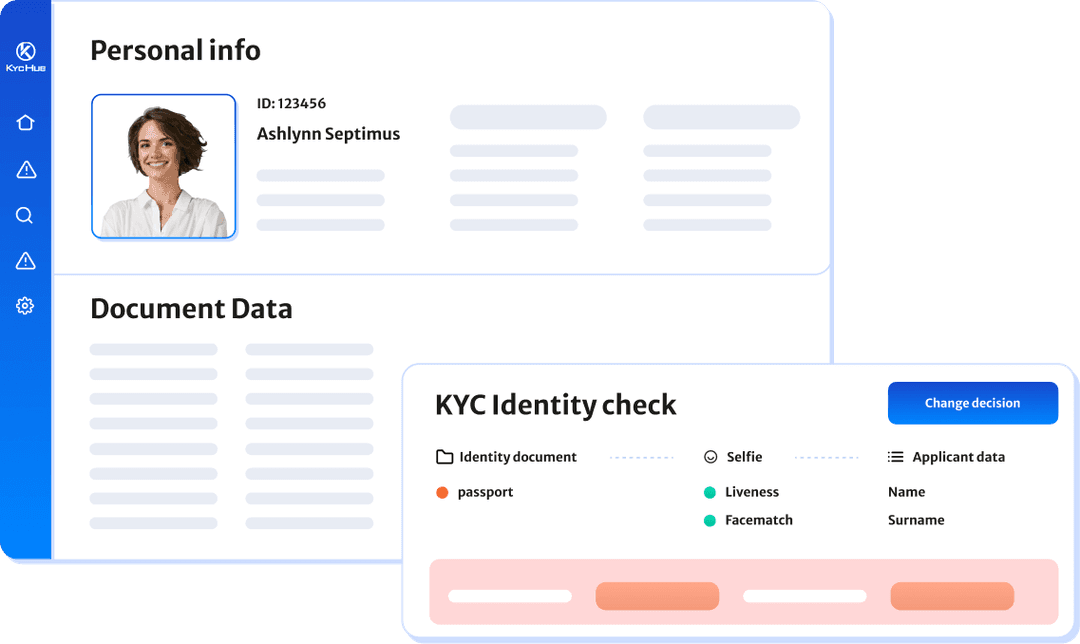

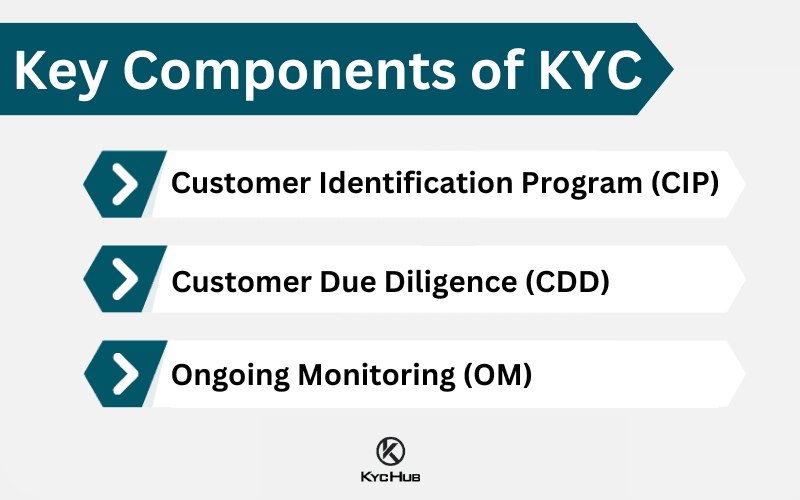

- Customer Identification Program (CIP): As mentioned earlier, the CIP involves collecting basic customer information, such as name, date of birth, address, and identification number. Financial institutions must also verify the customer’s identity by comparing the provided information with documents, such as a passport, driver’s license, or Social Security card.

- Customer Due Diligence (CDD): The CDD process involves collecting more detailed information about the customer, including their financial history, source of funds, and the intended nature of their business relationship. This helps financial institutions assess the risk associated with the customer and determine if they are involved in illicit activities.

- Ongoing Monitoring: Financial institutions must continuously monitor their customers’ transactions and activities to ensure they remain compliant with regulations and that their risk profile remains unchanged. This may involve reviewing account activity, conducting periodic reviews, and updating customer information.

- Reporting and Recordkeeping: Financial institutions must maintain records of their KYC processes, including customer identification and KYC verification documents, risk assessments, and transaction monitoring. They must also report any suspicious activities to the appropriate regulatory authorities.

KYC Hub Global KYC Solutions

What are the 4 Stages of KYC?

KYC (Know Your Customer) typically involves four key stages.

KYC Stages are:

- Customer Identification Program (CIP): The CIP requires financial institutions and other regulated entities to obtain and verify certain information, such as the customer’s name, address, date of birth, and identification documents like a passport or driver’s license.

- Customer Due Diligence (CDD): This element involves conducting a risk assessment of the customer to determine the level of risk they pose.

- Ongoing Monitoring: This element of KYC involves reviewing and updating customer information on a regular basis, as well as conducting periodic reviews of customer risk levels.

- Risk Management: Risk management also involves training employees on the KYC process and ensuring that they understand the importance of compliance.

KYC Key Components

When you think about Know Your Customer, you may wonder what exactly it entails. What are the key components that make up this process? Well, there are three main aspects to consider:

- Customer Identification Program (CIP): This is the first step in the KYC process, where financial institutions gather basic information about their customers. The CIP requires businesses to collect and verify the customer’s identification, such as name, date of birth, address, and identification number (e.g., Social Security number, passport number).

- Customer Due Diligence (CDD): Customer Due Diligence (CDD) goes beyond the primary identification of customers, delving deeper into their financial history, source of funds, and the intended nature of their business relationship. This step helps financial institutions assess the risk associated with a customer, ensuring that they are not involved in illicit activities.

- Ongoing Monitoring: The Know Your Customer process continues once the customer is onboarded. Financial institutions must continuously monitor their customers’ transactions and activities, ensuring that they remain compliant with regulations and that their risk profile remains unchanged.

Integrating Anti-Money Laundering (AML) measures into the KYC process enhances the ongoing monitoring of customer activities. This KYC AML synergy strengthens compliance, fortifies defenses against financial crimes, and fosters a safer, more transparent financial ecosystem.

The Importance of the KYC Process in the Financial Industry

Know Your Customer is crucial in the financial industry as a foundational element for risk management and regulatory compliance. Financial institutions must adhere to strict Know Your Customer regulations to protect themselves from potential losses and reputational damage.

Here are some key reasons why Know Your Customer is so important:

- Preventing Financial Crimes: Know Your Customer helps financial institutions identify and prevent financial crimes, such as money laundering, terrorist financing, and fraud. By verifying the identity of customers and assessing their risk, businesses can better detect suspicious activities and take appropriate action.

- Regulatory Compliance: Financial institutions must comply with various regulations to protect the financial system’s integrity. KYC is a critical component of these regulations, ensuring that businesses know who they are dealing with and can demonstrate their compliance to regulators.

- Risk Management: Know Your Customer enables financial institutions to better manage risk by identifying high-risk customers and implementing appropriate controls. This helps businesses minimize their exposure to potential losses and reputational damage.

KYC Documents

KYC documents can vary depending on the industry and the type of customer being verified. However, some common types of KYC documents include the following:

- Government-issued ID (such as a passport or driver’s license)

- Proof of address (such as a utility bill or bank statement)

- Tax identification number (such as a Social Security number or national ID number)

- Business registration documents (such as a certificate of incorporation or business license)

These documents are typically used to verify the customer’s identity and ensure that they are not on any watchlists or blacklists. In meeting the ‘Know Your Customer’ requirements, these essential documents not only ascertain the customer’s identity but also provide a foundation for a transparent business relationship.

When did KYC Verification Start?

The concept of verifying customers before commencing a business relationship, known as KYC, originated in the 1970s in the United States. It was initially drafted as a part of the Bank Secrecy Act (BSA) to combat money laundering. Since then, KYC requirements have evolved significantly. Notably, after the September 11th terrorist attack in 2001, the Patriot Act and the financial crisis of 2008 prompted substantial revisions.

These adaptations in KYC procedures were driven by a need for more proactive security measures, aiming to eliminate the risk of engaging with high-risk or illegitimate customers. Today, KYC compliance stands as a critical component of financial institution’s efforts to prevent financial crime and uphold the integrity of the global financial system.

KYC Regulations and Compliance

As mentioned earlier, many industries are required by law to perform KYC on their customers. Failure to comply with these regulations can result in hefty fines and legal consequences.

Some of the key regulations around KYC include the following:

- The USA PATRIOT Act (US)

- The Bank Secrecy Act (US)

- The Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017 (UK)

- The Prevention of Money Laundering Act, 2002 (PMLA) (India)

Know Your Customer regulations vary from country to country, but they generally share a common objective: to protect the financial system’s integrity and prevent financial crimes. Financial institutions must comply with these regulations or face penalties, including fines, sanctions, and even the loss of their operating license.

Some of the key regulatory bodies and frameworks governing KYC include:

- Financial Action Task Force (FATF): The FATF is an intergovernmental organization that develops and promotes policies to combat money laundering, terrorist financing, and other financial crimes. Its recommendations are the global standard for KYC and AML measures.

- Bank Secrecy Act (BSA): The BSA is the primary legislation governing KYC and AML requirements in the United States. Financial institutions must establish and maintain a Customer Identification Program (CIP) and report suspicious transactions to the Financial Crimes Enforcement Network (FinCEN).

- European Union (EU) Anti-Money Laundering Directives: The EU has implemented a series of AML directives to prevent money laundering and terrorist financing. These directives outline the KYC and AML requirements that financial institutions must adhere to within the EU.

- Other National Regulations: Besides the FATF, BSA, and EU directives, individual countries have Know Your Customer regulations and requirements. Financial institutions must familiarize themselves with the rules in each jurisdiction and ensure they remain compliant.

Complying with KYC laws and regulations are non-negotiable aspects of operating in today’s global financial landscape. As the penalties for non-compliance escalate, a thorough understanding of these regulatory standards not only aids in averting potential legal consequences but also fortifies the institutions against threats posed by fraudsters.

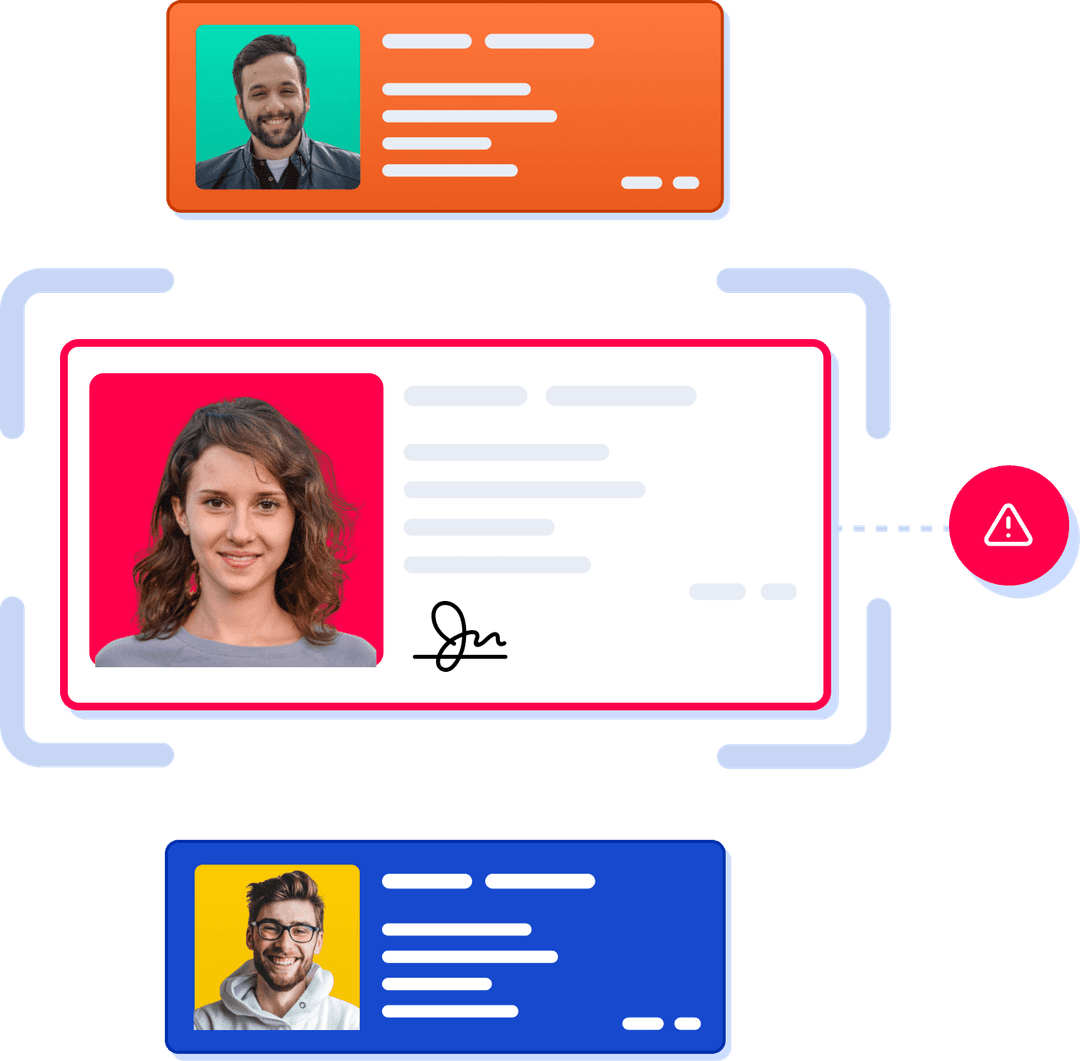

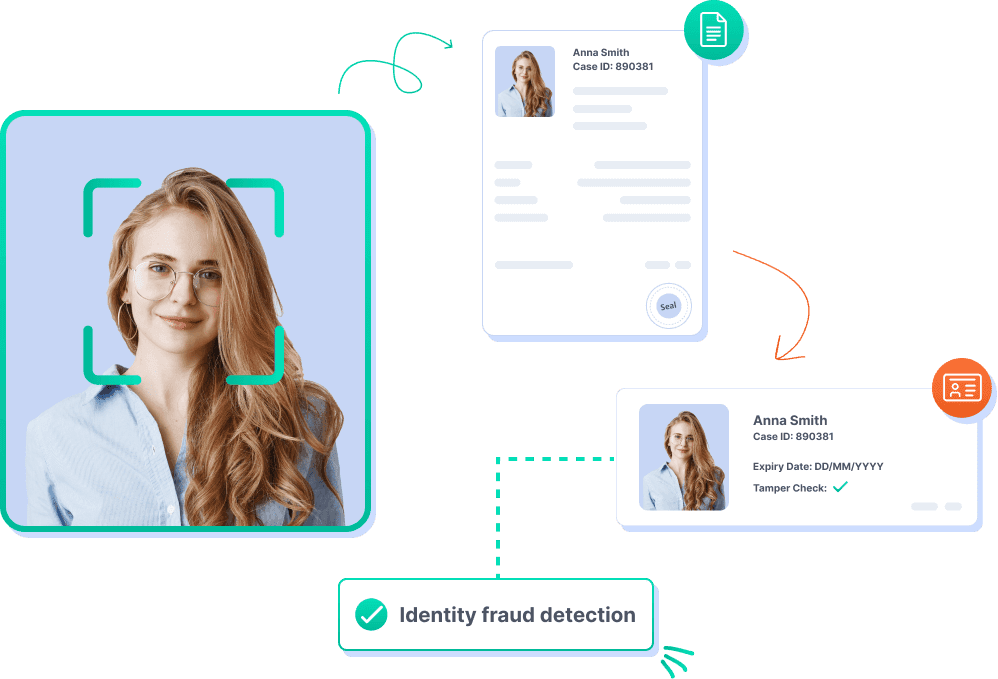

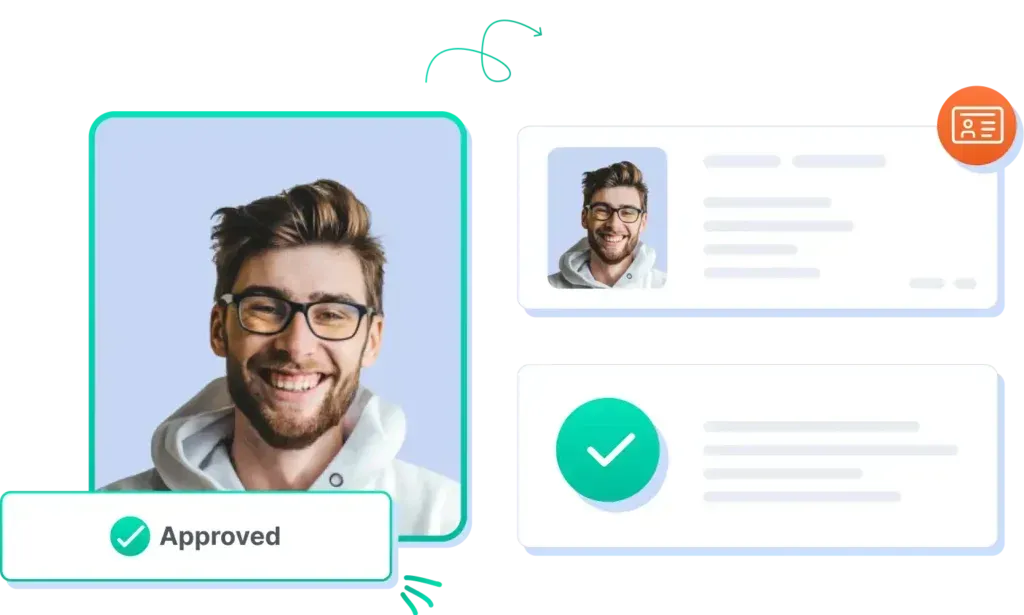

What is KYC Verification?

KYC verification is vital to preventing financial crime. The IFC suspects that robust KYC verification can improve CDD in smaller or more difficult emerging markets. Inaccurate or incomplete KYC verification can lead to criminals using financial institutions to launder money, finance terrorism, or commit fraud. The risks associated with financial crime include reputational damage, legal action, fines, and even imprisonment. Therefore, reliable KYC verification is essential for financial institutions to comply with AML regulations, prevent financial crime, and build trust with their customers.

Risks Associated with Inaccurate KYC Verification

- Inaccurate KYC compliance can expose financial institutions to significant risks, including legal and regulatory risks, financial risks, and reputational risks. These risks can have severe consequences for financial institutions and their customers.

- Legal and regulatory risks arise when financial institutions fail to comply with AML regulations. KYC verification is a critical component of anti-money laundering compliance, and failure to conduct accurate KYC verification can result in regulatory fines, sanctions, and legal action. Regulatory fines can be substantial, often running into millions of dollars, and can severely impact a financial institution’s profitability and reputation.

- Financial risks arise when financial institutions are used to facilitate financial crime. Criminals use financial institutions to launder money, finance terrorism, or commit fraud, among other illegal activities. When financial institutions fail to conduct accurate customer due diligence, they become vulnerable to these risks. This can result in significant financial losses that can impact the institution’s financial stability.

- Reputational risks arise when financial institutions fail to protect their customers’ assets and information. Inaccurate KYC verification can result in criminal activity, damaging the institution’s reputation and eroding customer trust. Customers are unlikely to do business with an institution that has a poor reputation, which can result in lost revenue and market share. Furthermore, a damaged reputation can take years to recover, resulting in long-term damage to the institution’s brand and profitability.

- Financial institutions face legal and regulatory risks, financial risks, and reputational risks when they fail to conduct accurate KYC verification. These risks can have significant consequences for financial institutions and their customers, making it crucial for financial institutions to have reliable KYC verification procedures in place.

Factors That Affect KYC Verification Reliability

Several factors can affect the reliability of KYC verification. These factors include data accuracy and completeness, the quality of data sources, verification processes and procedures, and the training and expertise of Know Your Customer verification personnel.

1. Data Accuracy and Completeness: Data accuracy and completeness are crucial factors in ensuring reliable KYC identity verification. Inaccurate or incomplete data can result in incorrect identity verification, making financial institutions vulnerable to financial crime. Therefore, financial institutions must ensure that they collect accurate and complete data during the KYC verification process.

2. Quality of Data Sources: The quality of data sources also plays a significant role in KYC verification reliability. Data sources must be reliable, trustworthy, and up-to-date. Financial institutions must have access to high-quality data sources to ensure accurate and reliable KYC verification.

3. Verification Processes and Procedures: Verification processes and procedures are also critical to ensuring reliable KYC verification. Financial institutions must have well-defined and effective identity verification processes and procedures in place for customer onboarding. These processes and procedures should be regularly reviewed and updated to reflect changes in regulations, technology, and best practices.

4. Training and Expertise of KYC Verification Personnel: The training and expertise of KYC verification personnel are essential to ensuring reliable KYC verification. KYC verification personnel must have the necessary training and expertise to conduct accurate identity verification. Financial institutions must invest in the training and development of their KYC verification personnel to ensure they have the knowledge and skills required to conduct reliable KYC verification.

As we see, several factors can affect the reliability of KYC verification. Data accuracy and completeness, the quality of data sources, verification processes and procedures, and the training and expertise of KYC verification personnel are all critical factors in ensuring accurate and reliable KYC verification.

Financial institutions must ensure they have effective processes and procedures in place and invest in the training and development of their KYC verification personnel to mitigate these factors’ impact on KYC verification reliability.

Best Practices for Ensuring KYC Verification Reliability

Financial institutions can ensure KYC verification reliability by following best practices. These best practices include establishing clear policies and procedures for KYC verification, using reliable data sources and verification tools, regularly updating and maintaining customer data, and providing ongoing training and support for KYC verification personnel.

1. Establishing clear policies and procedures for KYC verification: Establishing clear policies and procedures for KYC verification is essential for ensuring reliable KYC verification. These policies and procedures should be well-defined, documented, and communicated to all personnel involved in the KYC verification process.

This ensures that everyone is aware of their roles and responsibilities and that the KYC verification process is consistently applied. The FATF also recommends that the same clarity be extended to how existing policies can affect emerging technologies.

2. Using reliable data sources and verification tools: Using reliable data sources and verification tools is another best practice for ensuring reliable KYC verification. Financial institutions should have access to high-quality data sources that are regularly updated to ensure accuracy. They should also use reliable verification tools that can detect fraudulent activity and identity theft.

3. Regularly updating and maintaining customer data: Regularly updating and maintaining customer data is also critical to ensuring fraud detection. Financial institutions should have procedures in place for regularly updating and verifying customer data. This includes verifying customer identities and ensuring that customer data is accurate and up-to-date.

4. Providing ongoing training and support for KYC verification personnel: Providing ongoing training and support for KYC verification personnel is another best practice for ensuring reliable KYC verification. Financial institutions should invest in the training and development of their KYC verification personnel to ensure they have the necessary knowledge and skills to conduct accurate identity verification. Ongoing training and support also ensure that personnel are aware of changes in regulations, technology, and best practices.

Financial institutions can ensure KYC verification reliability by following best practices. These best practices include establishing clear policies and procedures for KYC verification, using reliable data sources and KYC verification software, regularly updating and maintaining customer data, and providing ongoing training and support for KYC verification personnel.

By implementing these best practices, financial institutions can mitigate the risks associated with inaccurate KYC verification and protect their customers from financial crime.

The Role of Technology in KYC Verification Reliability

- KYC technology plays a crucial role in improving the accuracy and reliability of KYC verification. It helps financial institutions collect and analyze customer data more efficiently and accurately, detect and prevent fraud, automate the KYC verification process, and comply with regulations and guidelines.

- By automating data collection, document verification, and risk management, KYC technology can help reduce the time and cost of KYC verification while ensuring consistency and compliance. It can also use advanced algorithms to extract data from customer documents and verify its accuracy, reducing the risk of human error. Additionally, KYC technology can use machine learning and artificial intelligence algorithms to identify fraudulent activities and detect suspicious patterns in customer behavior, preventing fraudulent activities and protecting financial institutions and their customers from financial crime.

- KYC technology can help financial institutions improve the reliability of KYC verification and mitigate the risks associated with inaccurate or incomplete KYC verification. By leveraging technology, financial institutions can ensure that their KYC verification process is accurate, efficient, and compliant with applicable laws and regulations.

Examples of KYC in Different Industries

KYC is used in several industries, including banking, finance, e-commerce, and telecommunications. Here are a few examples of how KYC is used in these industries:

- Banking: Banks are legally required to perform KYC on all their customers. This typically involves collecting and verifying customer information, such as name, address, and date of birth. Banks may also use additional KYC measures, such as biometric authentication or background checks.

- Finance: Investment firms and other financial institutions must also perform KYC on their customers. This helps prevent money laundering and other illegal activities.

- E-commerce: Many e-commerce companies now require KYC for certain transactions, such as high-value purchases or international orders. This helps prevent fraud and ensures customers are who they claim to be.

- Telecommunications: Telecom companies may require KYC for customers who are applying for postpaid plans or purchasing high-end devices. This helps prevent fraud and ensures that customers can pay their bills.

KYC across Different Countries

1: KYC process in the UK

In the UK, KYC is governed by the Money Laundering, Terrorist Financing, and Transfer of Funds (Information on the Payer) Regulations 2017 (MLR 2017). Under these regulations, businesses are required to perform KYC on their customers and to keep records of these checks.

The KYC process in the UK typically involves collecting and verifying customer information, such as name, address, and date of birth. This information is then compared to databases and public records to ensure the customer is who they claim to be. Businesses may also use additional KYC measures, such as biometric authentication or background checks.

2: KYC process in the US

In the US, the Know Your Customer process is governed by several regulations, including the USA PATRIOT Act and the Bank Secrecy Act. These regulations require financial institutions to perform KYC on their customers and report suspicious activity.

The KYC process in the US typically involves collecting and verifying customer information, such as name, address, and date of birth. This information is then compared to databases and public records to ensure the customer is who they claim to be. Financial institutions may also use additional KYC measures, such as biometric authentication or background checks.

3: KYC process in India

In India, KYC is governed by the Prevention of Money Laundering Act, 2002 (PMLA) and the Reserve Bank of India’s KYC guidelines. These regulations require businesses to perform KYC on their customers and to keep records of these checks.

The KYC process in India typically involves collecting and verifying customer information, such as name, address, and date of birth. This information is then compared to databases and public records to ensure the customer is who they claim to be. Businesses may also use additional KYC measures, such as biometric authentication or background checks.

Explore KYC Process & Requirements for other Countries-

KYC Solutions and Technology

As the Know Your Customer process becomes more complex and challenging due to increasing regulatory requirements and the growing risk of financial crimes, businesses are turning to technology and innovative solutions to streamline their KYC efforts. Some of the critical technologies and solutions used in the KYC process include:

- Digital Identity Verification: With the rise of digital technology, businesses can now verify the identity of their customers remotely and in real time using advanced tools like facial recognition, biometrics, and electronic document verification.

- Artificial Intelligence (AI) and Machine Learning (ML): AI and ML technologies can analyze large volumes of data and detect suspicious patterns and activities that may indicate financial crimes.

- Blockchain Technology: Blockchain technology can be used to create a secure and decentralized system for storing and sharing customer data, ensuring that it remains tamper-proof and protected from unauthorized access.

- Regtech Solutions: Regulatory technology, or Regtech, refers to using technology to streamline regulatory compliance processes. Regtech solutions can help financial institutions automate various aspects of the KYC process, such as customer identification, risk assessment, and reporting.

These technologies and solutions can help financial institutions improve the efficiency and accuracy of their KYC processes, reducing the risk of errors and delays while also enhancing compliance and risk management.

Challenges in Implementing KYC

Despite its importance, implementing a KYC system can be challenging for businesses. Some of the key challenges they may face include:

- Cost and Complexity: KYC can be costly and time-consuming, requiring significant resources and investment to implement and maintain. Small businesses, in particular, may need help to meet the regulatory requirements for KYC.

- Data Privacy and Security: Collecting and storing customer data can pose significant risks to data privacy and security, particularly with the rise of cyber threats and data breaches. Financial institutions must take appropriate measures to protect customer data from unauthorized access and ensure compliance with data protection regulations.

- Customer Experience: The KYC process can be cumbersome and frustrating for customers, leading to long wait times and delays. Financial institutions must find ways to balance regulatory compliance with a positive customer experience.

- Global KYC Requirements: With a globalized financial system, financial institutions must navigate a complex web of Know Your Customer regulations and requirements across different jurisdictions, making compliance a significant challenge.

Despite these challenges, implementing a robust KYC system is essential for financial institutions to protect themselves and their customers from financial crimes and regulatory penalties.

Technology and Tools to Streamline KYC Processes

To overcome some of the challenges associated with KYC, financial institutions can leverage various technologies and tools to streamline their processes. Some of the key technologies and tools used to simplify KYC include:

- Digital Onboarding Platforms: Digital onboarding platforms can help financial institutions automate the customer onboarding process, reducing wait times and improving the customer experience. These platforms can integrate with other KYC solutions, such as digital identity verification and risk assessment tools.

- Data Analytics and Visualization Tools: Data analytics and visualization tools can help financial institutions analyze large volumes of customer data, enabling them to identify patterns and trends that may indicate financial crimes.

- Regulatory Reporting Solutions: Regulatory reporting solutions can help financial institutions automate their reporting processes, ensuring compliance with KYC regulations and reducing the risk of errors and penalties.

- Blockchain-Based KYC Solutions: Blockchain-based KYC solutions can provide a secure and decentralized system for storing and sharing customer data, ensuring compliance with data protection regulations and reducing the risk of data breaches.

By leveraging these technologies and tools, financial institutions can streamline their KYC processes, reduce the risk of errors and delays, and enhance compliance and risk management.

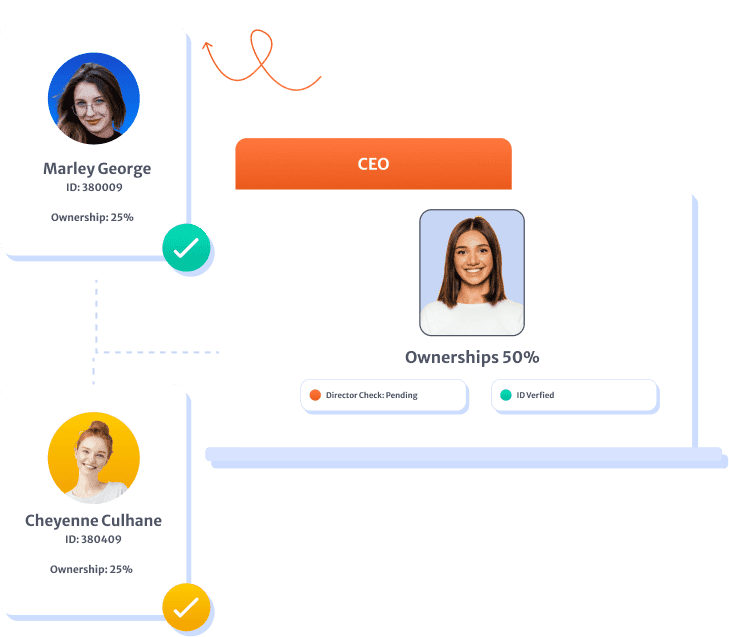

What is Corporate KYC?

Corporate KYC is the process of vetting a business or corporate entity along with its beneficiary owners.

It is an essential part of KYC compliance, focusing on authenticating and validating the identities of companies rather than individuals and ensuring compliance with Anti-Money Laundering (AML) and KYC regulations. This process aims to establish the legitimacy of businesses, including checks on Ultimate Beneficial Owners (UBOs) and other relevant information, to ensure compliance with industry regulations.

With the tightening of global regulations against money laundering and financial crimes, businesses and financial institutions are required to adhere to more rigorous KYC policies. Corporate KYC ensures this by verifying company registration documents and tax numbers, and may also require beneficiaries to provide personal information like passport numbers or ID cards.

How does KYC Work?

Corporate KYC services utilize company registration documents to obtain necessary information and validate it against a global database. The results of the screening are typically delivered via email or instant message. Automation tools can also generate a corporate risk score for clients, allowing for the daily monitoring of transactions based on this score. This enables businesses to allocate more time and resources to analyzing high-risk transactions or accounts.

Importance of KYC in Today’s Business Landscape

As financial crimes and regulatory requirements grow, KYC has become increasingly important in today’s business landscape. With the rise of digital technology and globalized financial transactions, businesses must take appropriate measures to protect themselves and their customers from potential risks.

A robust KYC system can help businesses achieve the following:

- Compliance with Regulations: By implementing a robust KYC system, businesses can ensure compliance with KYC regulations and avoid potential penalties and reputational damage.

- Risk Management: KYC enables businesses to assess customer risk and implement appropriate controls to minimize potential losses and reputational damage.

- Better Customer Experience: By leveraging technology and innovative solutions, businesses can streamline their KYC processes, reducing wait times and improving the customer experience.

- Enhanced Security: KYC can help businesses protect customer data from unauthorized access and ensure compliance with data protection regulations.

Overall, KYC is essential to today’s business landscape, enabling businesses to protect themselves and their customers from potential risks while enhancing compliance, risk management, and customer experience.

KYC Best Practices

To ensure that your Know Your Customer process is effective and compliant, here are a few best practices to follow:

- Keep up-to-date records: Ensure that you keep accurate records of all KYC checks and update these records regularly.

- Use multiple verification methods: Use various verification methods, such as biometric authentication and background checks, to ensure that you accurately verify customer information.

- Train your staff: Ensure that your staff is properly trained on Know Your Customer procedures and understands the importance of KYC compliance.

- Use KYC software: Consider using KYC software to help streamline the KYC process and improve accuracy.

Benefits of a Robust KYC System

A robust KYC system can provide numerous benefits for businesses, including:

- Improved Compliance: A robust KYC system can help businesses comply with Know Your Customer regulations, reducing the risk of penalties and reputational damage.

- Enhanced Risk Management: KYC enables businesses to assess customer risk and implement appropriate controls, minimizing potential losses and reputational damage.

- Increased Efficiency: By leveraging technology and innovative solutions, businesses can streamline their KYC processes, reducing wait times and improving efficiency.

- Better Customer Experience: A streamlined KYC process can enhance the customer experience, reducing wait times and improving convenience.

- Enhanced Security: A robust KYC system can help businesses protect customer data from unauthorized access and ensure compliance with data protection regulations.

By implementing a robust KYC system, businesses can achieve these benefits and enhance their compliance, risk management, and customer experience.

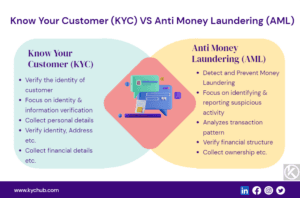

KYC and AML Measures [KYC vs AML]

KYC is closely tied to AML (Anti-Money Laundering) measures, as KYC and AML both are designed to prevent financial crimes and protect the financial system’s integrity. AML measures encompass a broader range of activities, including detecting and reporting suspicious transactions, conducting risk assessments, and implementing appropriate controls.

KYC is a critical component of AML measures, enabling businesses to verify the identities of their customers and assess the risks associated with them. By implementing a robust KYC system, companies can enhance their AML measures and reduce the risk of financial crimes.

Future Trends in KYC and CDD [KYC vs CDD]

As the financial industry evolves, so will Know Your Customer and customer due diligence practices. Some of the key trends to watch in this space include:

- Digital Identity Verification: The use of digital identity verification tools will become increasingly prevalent as businesses look to streamline their KYC processes and improve the customer experience.

- AI and ML Technologies: AI and ML technologies will become more widespread, enabling businesses to analyze large volumes of customer data and detect suspicious activities more effectively.

- Regulatory Technology (Regtech): The adoption of Regtech solutions will continue to grow, enabling businesses to automate various aspects of the KYC process and enhance compliance and risk management.

- Blockchain Technology: Blockchain-based KYC solutions will become more prevalent, providing a secure and decentralized system for storing and sharing customer data.

- Collaboration and Standardization: Financial institutions will increasingly collaborate and standardize their KYC processes, reducing compliance’s complexity and cost and enhancing AML measures’ effectiveness.

As these trends continue to shape the future of Know Your Customer and customer due diligence, businesses must stay up-to-date with the latest developments and adopt appropriate measures to protect themselves and their customers.

KYC Hub Global KYC Solutions

Conclusion

Know Your Customer is a critical process for financial institutions and businesses, enabling them to verify the identity of their customers and assess the risks associated with them. With the growing risk of financial crimes and regulatory requirements, implementing a robust KYC system is essential for businesses to protect themselves and their customers.

By leveraging technology and innovative solutions, businesses can streamline their KYC processes, reduce the risk of errors and delays, and enhance compliance and risk management. As the financial industry evolves, businesses must stay up-to-date with the latest developments in KYC and customer due diligence and adopt appropriate measures to protect themselves and their customers. Get in touch to check out our advanced Know Your Customer solutions.

KYC Hub offers reliable data sources, verification tools, and regularly updated and maintained customer data. KYC Hub’s technology solutions are designed to improve verification accuracy and reliability, helping financial institutions ensure AML compliance while streamlining their processes. With KYC Hub, companies can benefit from a comprehensive and customizable KYC verification service that meets their unique needs and requirements.