What Documents are Required for KYC in India? [KYC Documents]

![What Documents are Required for KYC in India? [KYC Documents]](/_next/image?url=https%3A%2F%2Fpub-97215677d22e4f79a6fa7ef427da4388.r2.dev%2Fmedia%2Fdocuments-required-for-kyc-in-india-3.jpg&w=3840&q=75)

Key takeaways

- Indian KYC requires an Officially Valid Document (OVD): Aadhaar, PAN, passport, voter ID or driver's licence — most institutions accept Aadhaar plus PAN as the standard pair.

- Three RBI-approved paths exist: paper KYC (in-person), e-KYC (Aadhaar OTP, online) and V-CIP (live video call). Customers can move between paths during the customer lifecycle.

- Address proof, a recent photograph and a signed declaration are mandatory across paths; documents must be self-attested or biometrically verified depending on the channel.

The documents required for KYC in India play a pivotal role in verifying customer identities and safeguarding the country’s financial system. KYC’s significance in this dynamic arena cannot be overstated, as it serves as the linchpin that fortifies the financial ecosystem against a myriad of risks.

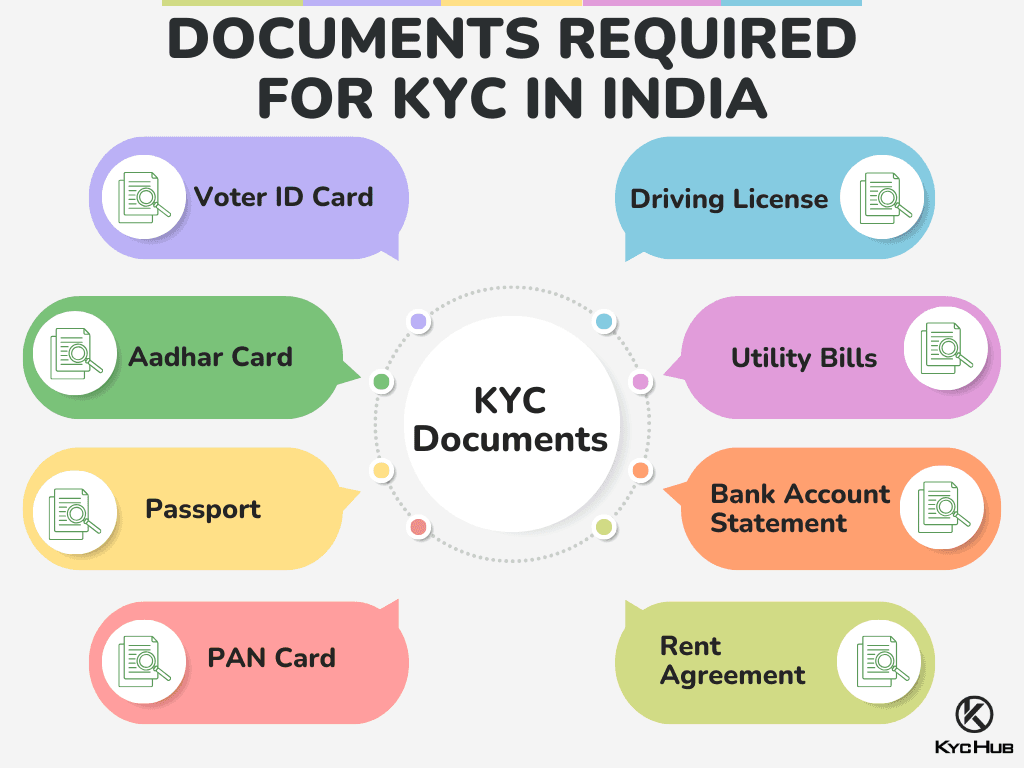

The documents required for KYC in India typically include government-issued photo ID proof, such as an Aadhar card, passport, voter’s ID, or driver’s license. Additionally, proof of address, like utility bills or bank statements, is necessary for completing the KYC process in India.

KYC, which means Know Your Customer, refers to a collection of precisely created rules and procedures that are used to confirm the identity of people or entities engaging in financial transactions. At its core, its main goal is to make sure financial institutions have a thorough grasp of their clients. KYC compliance has become a potent weapon as fraudsters and money launderers increasingly target financial institutions.

What are KYC documents?

KYC (Know Your Customer) documents are the identity and address proofs that verify a customer’s identity and address to prevent fraud, money laundering, and financial crime. This includes government-issued IDs (passport, driver’s license, national ID card), proof of address (utility bills, bank statements, rental agreements), and sometimes biometric verification or photographs.

Banks, fintech companies, cryptocurrency exchanges, and financial institutions require KYC documents for account opening and transparency in transactions.

Examples of KYC documents

KYC Documents are;

- Aadhaar card

- PAN card

- Voter ID card

- Driver’s license

- Utility bill

- Passport

- Ration card

By meticulously verifying customer identities and scrutinizing their financial activities, KYC acts as a formidable barrier against money laundering, terrorist financing, and fraudulent schemes. Shedding light on the profound significance of KYC within the financial sector, today we discuss the documents necessary for updated KYC verification in India. Compliance teams that process thousands of documents a month rely on intelligent document processing to extract, classify, and validate ID and address proofs in seconds instead of minutes.

Know Your Customer India Process

Before we can delve into what documents are needed in India for online KYC verification, it is perhaps most important to first understand the KYC verification process itself. KYC isn’t merely a regulatory requirement; it’s a shield that fortifies the financial ecosystem against the ever-looming threats of money laundering, terrorist financing, and financial fraud. For regulated entities, RBI's V-CIP rules also permit document collection over a live video call — see video KYC for the operational details.

As we navigate through the intricate layers of KYC, we’ll gain insights into why it stands as an indispensable element in safeguarding the integrity and trustworthiness of financial transactions.

KYC acts as the cornerstone upon which financial institutions construct a secure and open financial ecosystem by thoroughly validating customer identities.

Completing the KYC process is essential for various financial transactions, including opening bank accounts, investing in fixed deposits, recurring deposits, mutual funds, and more. It helps in verifying the identity and background of customers to prevent financial fraud and money laundering.

KYC documents include a wide range of identity and address verification methods that combine to represent an individual with accuracy. Under the categories mentioned above, these documents all serve as tangible proof of individuals’ identities and ensure that financial institutions have a comprehensive understanding of their customers. This carefully curated list of accepted documents for KYC includes, but is not limited to:

The accepted KYC documents list for India are

For Individuals:

- Voter ID Card/Identity Card

- Aadhaar Card

- Passport

- Driving Licence

- PAN Card

- NREGA Card

- Letter issued by the National Population Register.

- Ration Card with a Photograph

Proof of Address:

- Aadhar Card

- Voter ID Card

- Driving Licence

- Recent utility bills (Water, Gas, Electricity)

- Rent agreement

- Passport

- Bank account statement or passbook with the latest transaction

For Corporate Entities:

- Certificate of Incorporation (COI)

- Board Resolution authorizing signatories

- Memorandum and Articles of Association

- PAN Card of the company

- Address proof of the company

- List of Directors and their KYC documents

- List of Shareholders and their KYC documents

For Partnership:

- Partnership Deed

- PAN Card of the partnership firm

- Registration certificate

- Address proof of a partnership firm

For Trusts and Societies:

- Registration Certificate

- Trust Deed

- PAN Card of trust

- List of Trustees/Committee members and their KYC documents

- Address proof of trust

For Sole Proprietorship:

- Business registration certificate

- PAN card of proprietorship

- Proof of address and identity of proprietorship

- Bank statement of business

Additional identity proof like:

- Identity documents issued by authorities: This covers a range of official documents with your picture on them that are published by various state and federal governments. These include identification cards issued by governmental regulatory/authority/statutory, state, or central agencies.

- Identity documents from educational institutions: These refer to identity cards issued by educational institutions that are affiliated with distinguished professional bodies such as the Institute of Company Secretaries of India (ICSI), the Institute of Cost Accountants of India (ICWAI), the Institute of Chartered Accountants of India (ICAI), and the Bar Council.

- Certified identity cards from financial institutions or employers: This category includes identity cards that have been certified by financial institutions or employers. It encompasses identity cards issued by scheduled commercial banks, public sector organizations, and private sector entities.

KYC Document in India for Compliance

In India, KYC compliance is not just a best practice; it’s a legal requirement for institutions like SBI. Financial institutions are mandated by law to follow KYC norms. These norms are governed by the Prevention of Money Laundering Act, of 2002, and enforced by the Reserve Bank of India (RBI). The legal requirements are comprehensive and detailed, leaving no room for ambiguity.

They place the onus on financial institutions to conduct due diligence, verify customer identities, and maintain meticulous records.

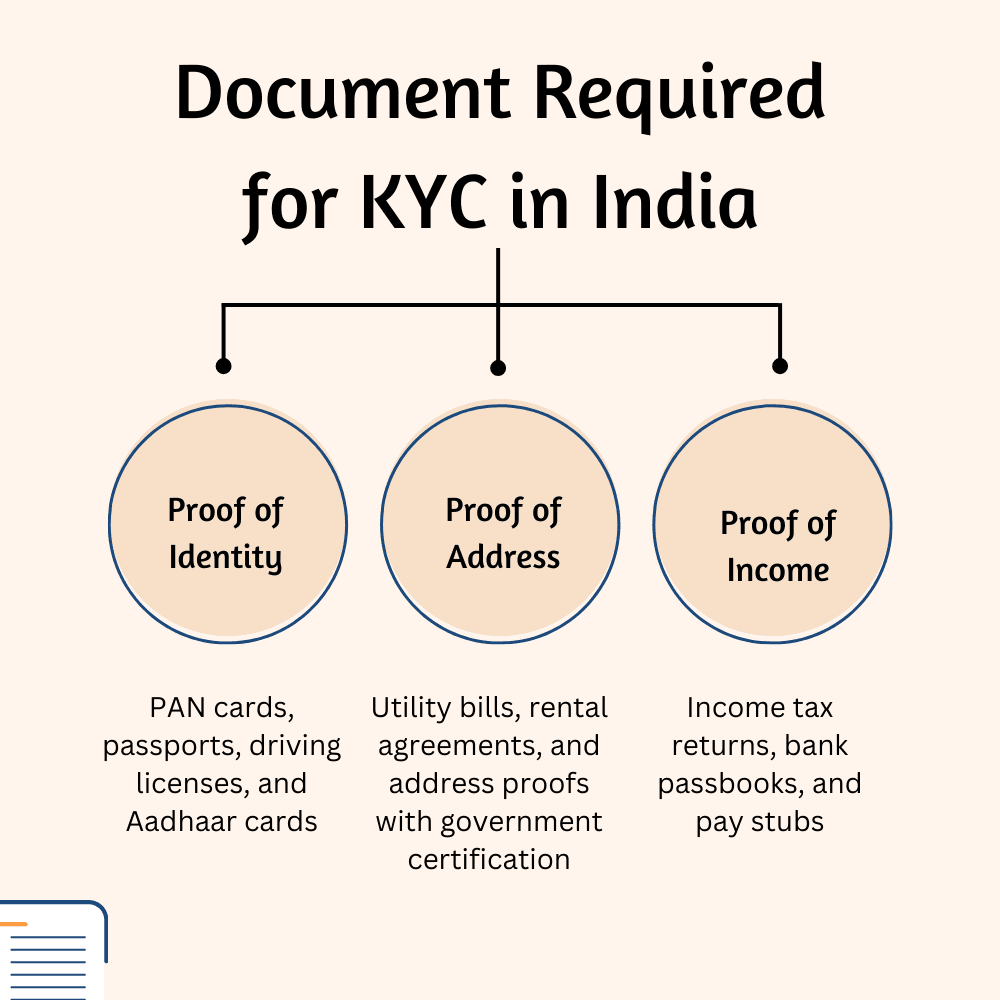

At the very core of its essential and secure system, KYC revolves around the types of documents individuals and institutions need to provide. These documents serve as the foundation upon which KYC verification is built, ensuring that financial transactions remain secure, transparent, and compliant with regulatory mandates. Thanks to a few key documents, the government can have a hefty record of each individual and their extensive financial history. The nature of these documents boils down to three key types:

1. Proof of Identity

In this category, documents like PAN cards, passports, driving licenses, and Aadhaar cards are crucial. They function as a reliable way to confirm a person’s identity because they contain crucial information, such as name, picture, and unique identification numbers.

2. Proof of Address

Documents proving an individual’s address are crucial for financial organizations to have a thorough overview of their clients. Utility bills, rental agreements, and proof of address with government certification are just a few of the documents that confirm a customer’s domicile and reveal information about their geographic presence.

3. Proof of Income

Knowing a customer’s financial situation is crucial for achieving thorough KYC compliance. Documents that shed light on a person’s financial situation include income tax returns, bank passbooks, and pay stubs. Financial organizations might use this category to evaluate a customer’s creditworthiness and risk profile.

Types of KYC India Verification

In a diverse country like India, the biggest driver of measures like KYC is to promote financial innovation and inclusion across the board. India, with its diverse population and unique challenges, employs various KYC online verification methods. Innovative approaches have emerged to meet the diverse needs of a vast and vibrant population. Two prominent ones accurately showcase this diversity and reach. They are:

1: Aadhaar-based KYC (eKYC)

This streamlined process leverages the unique Aadhaar identity issued by the Unique Identification Authority of India (UIDAI). It simplifies verification by utilizing Aadhaar details and biometric authentication, providing a standardized and widely accepted form of identification. eKYC has revolutionized the financial sector, enabling seamless and efficient online verification through internet connectivity.

2: In-person Verification (IPV) KYC

For individuals who prefer or require offline verification, IPV KYC offers a viable option. It involves physically visiting a financial institution or a KYC registration agency for identity verification. Though more traditional, IPV KYC ensures accessibility for those unable to undergo digital verification.

👉Related Read: Voter ID Verification in India: A Simplified Guide

Benefits of KYC

Now that we’ve addressed the need for KYC, it is also imperative to take a moment to understand the benefits it adds as well. Beyond just being a preventative force, KYC also brings a few unique advantages to the table. In this section, we examine the numerous advantages that KYC offers organizations and institutions, highlighting the reasons why it’s essential for success in contemporary finance.

1. Enhanced Security

KYC processes play a pivotal role in enhancing security for businesses and financial institutions. By meticulously verifying the identity of customers, organizations can ensure that only legitimate individuals or entities have access to their services. This prevents unauthorized access, minimizes the risk of fraud, and creates a robust defense against criminal activities like money laundering and identity theft.

2. Improved Trust and Reputation

KYC builds a foundation of trust between businesses and their customers. When individuals know that their identities are thoroughly verified, they are more likely to engage with businesses confidently. This trust is invaluable in attracting investments, fostering customer loyalty, and maintaining a positive reputation in the market.

3. Reduced Risk Exposure

Through KYC compliance, businesses can effectively manage risks associated with their customers. By gaining comprehensive insights into a customer’s financial history, background, and risk profile, organizations can make informed decisions regarding transactions, lending, and other financial services. This leads to reduced exposure to potential risks and helps in maintaining a healthy and secure business environment.

4. Efficient Customer Onboarding

KYC processes streamline the customer onboarding experience through various types of KYC verification processes. By utilizing electronic identity verification and document authentication, businesses can expedite the registration process. This improves operational efficiency and enhances the overall customer experience, making it more convenient and hassle-free.

5. Competitive Advantage

Having a robust KYC framework gives businesses a competitive edge in the market. It demonstrates a commitment to compliance, security, and responsible business practices. This can be a distinguishing factor for customers who prioritize security and trustworthiness when choosing service providers. Additionally, it positions businesses as reliable partners in the eyes of regulators and stakeholders.

6. Global Expansion Opportunities

Compliance with Many countries have stringent KYC requirements in place, and having a well-defined KYC process enables businesses to enter new markets with confidence. It demonstrates a commitment to compliance with international standards, making it easier to establish operations in different jurisdictions.

Addressing Risks Associated with Financial Crime

Failing to implement proper KYC measures can have dire consequences for individuals, financial institutions, and the broader financial landscape. To neglect or inadequately implement these measures is to open the floodgates to an array of perilous risks, with consequences that reverberate across the broader financial ecosystem.

The absence of comprehensive KYC safeguards leaves financial institutions susceptible to unwittingly becoming conduits for money laundering and terrorist financing operations. Insufficient identity checks may allow funds to slip through the cracks, financing acts of terror and casting a dark shadow over the institution’s reputation.

An insufficient KYC framework paves the way for criminals to seize the opportunity and engage in a spectrum of fraudulent activities.

The regulatory landscape is unforgiving when it comes to KYC adherence. Entities failing to meet these standards can find themselves facing punitive fines and sanctions along with crippling reputational damage. The uphill battle to regain a sterling reputation can be long and arduous, culminating in protracted legal battles that drain resources and undermine credibility.

But KYC isn’t merely a regulatory prerequisite; it stands as an indispensable fortress of the global financial ecosystem. Money laundering and fraudulent activities chip away at the very foundations of the financial system, eroding public faith and potentially triggering economic turmoil.

Conclusion

The KYC process stands as a critical line of defense against money laundering, fraud, and other illicit activities. KYC compliance in India is not just a requirement; it’s a powerful defense against financial crime. The documents for KYC in India play a pivotal role in verifying customer identities and safeguarding the financial system.

With KYC Hub as your partner, you can navigate these KYC requirements in India efficiently and confidently. Our expertise and cutting-edge solutions are designed to empower businesses to meet and exceed these compliance standards. By automating and streamlining the KYC process, we help you save valuable time and resources, allowing you to focus on core business activities. Let’s embark on this journey together, ensuring a secure and prosperous future for your business.