KYC for Fintech: A Compliance Playbook for Scaling Onboarding

KYC for fintech is the set of identity verification, due diligence, and ongoing monitoring controls a fintech runs to confirm who its customers are and to gauge the financial crime risk they carry. It exists to satisfy anti-money laundering law, keep fraudsters and sanctioned parties off the platform, and give regulators an auditable record of every onboarding decision. The concept is not the hard part. Doing all of it in seconds, at scale, across borders, without turning sign-up into a wall that legitimate customers abandon: that is the hard part.

That trade-off lands on compliance, risk, and product leaders, and this guide is written for them. You will find what KYC obligations actually require, where AML fits in, the onboarding and regulatory pressures fintechs face that banks largely do not, and the operational moves that let verification keep pace with a growth roadmap instead of fighting it.

Why KYC Matters More for Fintechs Than for Banks

Traditional banks built their KYC programs around branches, paper, and time. A fintech has none of those buffers. Customers arrive through an app, expect an account in minutes, and judge the brand on the first screen. Speed is the product. Speed is also the attack surface, because the smooth flow that wins customers is the one a money mule or synthetic identity ring probes first.

Most fintechs also operate across many jurisdictions before they have a mature compliance function, so a single onboarding flow has to honor several rule sets at once. Add embedded finance, where a fintech inherits KYC duties on behalf of partner programs, and the obligation surface grows faster than headcount. So KYC for fintech is rarely a one-time project. It has to absorb new products, markets, and fraud patterns as they arrive, which is why so many fintechs move to a perpetual KYC model instead of a periodic refresh cycle.

What KYC for Fintech Actually Requires

A defensible program comes down to a handful of controls that regulators expect to see documented and actually running, not just written into a policy.

Customer Due Diligence and Identity Verification

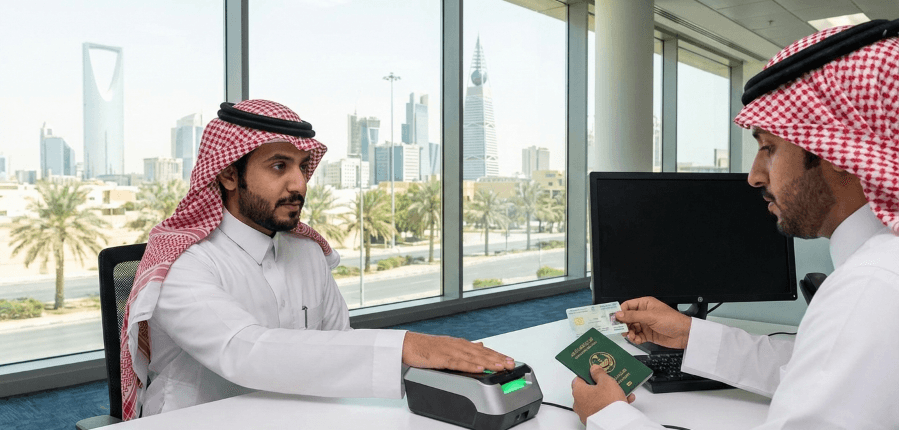

Customer due diligence sits at the core of any KYC program. You collect identifying information, verify it against reliable independent sources, and form a view of the customer's expected activity. For most fintechs this runs through automated identity verification that checks a government document, matches it to a live selfie, and confirms the person presenting the document is the genuine holder rather than a deepfake or a stolen image. Cover individuals, and for business accounts, cover the entities and beneficial owners behind them too.

Risk Assessment and Customer Risk Rating

Not every customer warrants the same scrutiny. A risk-based approach scores each one on factors such as geography, product, transaction profile, and exposure to politically exposed persons, and the depth of diligence follows from that score. Low-risk customers clear a streamlined path. Higher-risk profiles trigger enhanced due diligence and tighter monitoring. When a compliance team has to defend why one applicant sailed through while another got escalated, a consistent customer risk rating model is what holds up.

Ongoing Monitoring and Record-Keeping

KYC does not end at onboarding. Fintechs have to watch for changes that shift a customer's risk, from a fresh sanctions hit to a sudden swing in transaction behavior, and they must retain identification and decision records, typically for five years or more depending on the jurisdiction. That audit trail is the difference between a clean regulatory exam and a finding. Pairing onboarding with transaction monitoring closes the loop, so risk that emerges after account opening still surfaces.

Where AML Fits Into Fintech KYC

KYC is the entry point to a broader anti-money laundering obligation. AML law requires fintechs to screen customers against sanctions lists, watchlists, and politically exposed person databases, monitor transactions for suspicious patterns, and report suspicious activity to the relevant financial intelligence unit. None of that screening means much without a verified identity and a risk profile behind it, and KYC supplies both. Without reliable identity at the front, downstream AML screening just matches names against lists with no confidence the name belongs to the person on the account.

For fintechs the screening burden runs heavier, because customers and counterparties span many countries and lists. Run AML screening and monitoring against sanctions, watchlists, crime lists, and PEP data, with risk attributes you configure rather than accept off the shelf. Tuned well, that stops false positives from burying a lean compliance team while still catching genuine exposure.

The Fintech Onboarding Problem

Every percentage point of onboarding drop-off is revenue a fintech never sees, so the pressure to make verification invisible runs intense. Treating that pressure as a reason to weaken controls is the mistake. Make strong controls fast instead.

Modern fintech onboarding folds document capture, biometric liveness, and back-end screening into a single flow that resolves in minutes for most customers, leaving manual review for the cases that genuinely need it. The advantage comes from orchestration: route each applicant through only the checks their risk level demands, run those steps in parallel, and auto-clear the clean majority so analysts spend their time on the edge cases. When a platform handles document forensics across thousands of ID types and verifies identity across a wide range of countries, a fintech can open one onboarding flow to a global customer base instead of stitching together regional point tools.

Book a Demo to see how an orchestrated onboarding flow clears low-risk customers in seconds while routing the rest to review.

Fintech Regulatory Compliance Across Borders

Serve customers in multiple countries and you inherit multiple AML regimes, each with its own identity standards, record-keeping rules, reporting thresholds, and data protection law. Operating in the European Union, for instance, pulls in GDPR obligations on how customer data is collected, stored, and accessed. Expand into a new market and you can hit local verification requirements the existing flow does not satisfy. Keeping a single program coherent while honoring every jurisdiction it touches: that is the compliance team's job.

Configurability matters more here than any single feature. A program built on fixed rules breaks the moment a new market is added. Build it instead on workflows you adapt per jurisdiction, with the audit trail to prove each market's rules were applied, and it scales with the business instead of capping it. The same principle holds as products expand. Lending, payments, and crypto rails each carry their own diligence expectations, and automation is what keeps those obligations from outrunning the team.

KYC Challenges Specific to Fintechs

Several pressures land harder on fintechs than on incumbents. Name them, and a team can design controls that hold.

Fraud at speed comes first. Synthetic identities, document forgeries, and account takeover attempts are all built to exploit fast digital onboarding, so identity proofing has to catch manipulation in real time rather than after the fact. Build strong fraud prevention into the onboarding step, leaning on entity resolution and network analysis to spot rings rather than isolated bad actors. That is what separates a control that catches fraud from one that merely records it.

Then there is false-positive load. No lean compliance team can manually clear thousands of screening alerts, so a program that floods analysts with noise turns into a hiring problem dressed up as a compliance problem. Tuning risk attributes and resolving entities to cut duplicate and irrelevant hits is what separates a team that scales from one that drowns.

Third: the build-versus-buy trap. Many fintechs start by wiring together separate vendors for document checks, sanctions screening, and monitoring, then discover the seams between those tools are where risk and cost accumulate. A composable platform that exposes the pieces a fintech needs, without forcing a rip-and-replace, tends to age better than a hand-built stack.

How to Scale KYC Without Slowing Growth

Scaling KYC is an orchestration problem more than a headcount problem. Fintechs that get it right share a few habits. They automate the clean majority so humans only see exceptions. Effort matches exposure because they route by risk. With continuous monitoring, a customer who turns risky after onboarding does not sit unnoticed until the next review cycle. And they keep the whole flow configurable, so a new market or product does not force a rebuild.

KYC Hub's platform for fintech compliance is built around exactly these pillars: fast digital onboarding with biometrics and liveness, automated KYC and AML screening with configurable risk attributes, fraud prevention through entity resolution and network analysis, and a modular architecture that lets a fintech assemble only the controls it needs. The point is simple. A compliance team should be able to support aggressive growth targets without becoming the bottleneck the rest of the company works around.

Book a Demo to map your onboarding and screening stack to a configurable compliance platform built for fintech scale.