KYC Onboarding Process for Compliance in 2026

Digitisation changed how regulated firms take on customers, and the sharpest change hit the front door. What once meant photocopied documents and a wait of several days now resolves on a phone within minutes. Governing that first encounter is the KYC onboarding process. Below, we set out what the process involves, why it carries so much weight for compliance teams asked to onboard faster while keeping their controls tight, and what each stage requires in the way of documentation. Fundamentals have held steady over the years. How firms carry them out has changed beyond recognition.

Worth planning around in 2026 is a single structural shift: the one-time gate has gone. Onboarding has stopped being a checkpoint a customer clears once and forgets. Now it opens a continuous cycle. Perpetual KYC programmes reuse the data captured at signup to drive event-driven reviews, so a profile assembled with care on day one repays that effort for as long as the customer relationship lasts. Build it carelessly and the costs keep accruing the other way.

What is the KYC Onboarding Process?

Know Your Customer onboarding, usually shortened to KYC onboarding, is the way an organisation brings a new customer into its systems while confirming who that customer genuinely is. The sequence opens at account creation. Product orientation typically comes next. Handled properly, the whole journey raises satisfaction and retention at the same moment it meets the legal and regulatory duties that sit behind every regulated relationship.

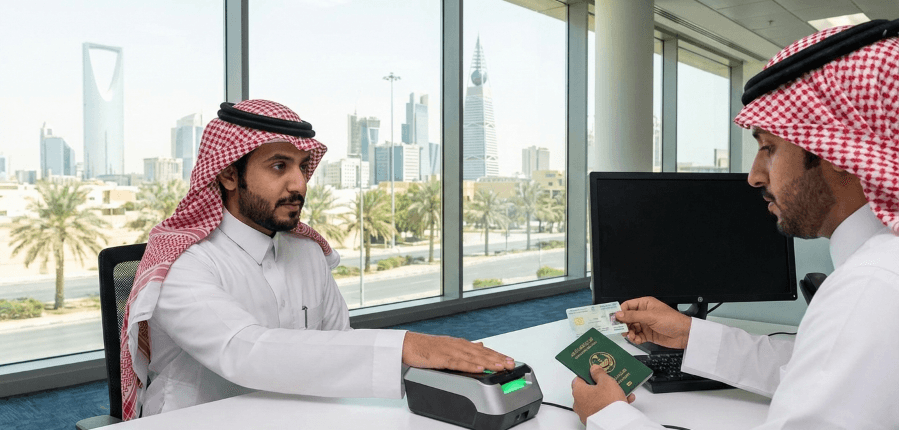

In regulatory terms, KYC onboarding is the set of checks a firm clears before it transacts with anyone new, and that same duty applies whether a customer walks into a branch, fills in a web form, or taps through a mobile app, with the channel making no difference to what the firm must establish. Two tasks anchor the work. A firm collects information about the customer, then it proves that information is real.

Baseline data a firm needs to identify an individual customer includes:

- Name

- Date of birth

- Address

KYC onboarding keeps firms inside anti-money laundering (AML) law. Which facts and which documents a firm must gather will differ from one jurisdiction to the next, so compliance teams ought to read the AML statutes and guidance for every market they serve, given how often the requirements move. Consider the European Union. The new Anti-Money Laundering Authority (AMLA) began operations in Frankfurt on 1 July 2025, and the directly applicable single rulebook under the Anti-Money Laundering Regulation applies from 10 July 2027, replacing a patchwork of national rules that firms once had to reconcile market by market.

Verification runs deeper. Firms have to obtain original, verifiable evidence directly from the customer. Usually that means a government identity document such as a passport or driver's licence, paired with proof of address (a utility bill, a tax notice, an entry on the electoral roll, or a recent bank statement).

Who needs KYC onboarding?

KYC duties reach across the whole economy, and they press hardest on businesses tied to money movement and financial services. For firms in those sectors, treating Know Your Customer onboarding as optional carries real consequences. Controls belong in place before the first transaction, because regulators judge a firm on what it did at the point of acceptance, well ahead of anything it later promises to fix. A few industries are caught most consistently:

- Financial Organizations and Banks

- Fintech Firms

- Businesses Specialized in Real Estate

- Accounting Companies and Legal Firms

- Online Marketplaces

- Sites for Gambling and Gaming

Capable onboarding gives these firms a transparent, defensible operating model. Fraud is stopped at the point of entry. Such a firm stays inside anti-money-laundering legislation, with its evidence already on file, well before an examiner asks why a particular account was approved at all and the firm finds itself reconstructing the answer. Preparation marks the divide between firms here. One has the answer ready. Another assembles it under pressure once the question arrives.

Difference between KYC and KYB Onboarding

KYC and KYB onboarding split along two lines: who each one examines, and how far each one digs.

- KYC onboarding deals with individual customers. KYB onboarding deals with corporate ones.

- KYC onboarding is comparatively straightforward, while KYB onboarding runs longer because mapping a company is harder than confirming a person.

- KYC onboarding confirms an individual's identity before that person opens an account or subscribes to a financial service.

- KYB instead traces a company's financial footprint, where its capital comes from, the AML risk it carries, and the ownership layers stacked above it, which take in any individual holding a 25 percent or greater stake.

- During KYC onboarding, a firm asks for personal identification documents, proof of address, and contact details.

- KYB onboarding goes well past that list, gathering company registration data, banking details, a risk assessment, evidence of AML compliance, and a full reading of organisational structure.

What is the difference between KYC and Client Onboarding?

Client onboarding is the wider act of welcoming someone into a business. Inside it is the narrower discipline that verifies and authenticates that someone, and that discipline is KYC onboarding. The overlap is large. Yet the two remain distinct. Treat them as one thing and a firm risks over-collecting data from low-risk customers or, at the other extreme, skipping verification steps the law genuinely requires for everyone else. Commercial preference does not set the trigger for a KYC requirement; regulation does, and a given client onboarding journey may carry no KYC obligation at all.

When a regulated firm runs client onboarding ahead of accepting a relationship, the verification layer it applies is Know Your Customer, or KYC. Three identifiers carry most of the weight. Name, date of birth, and address together pin a customer to a real identity, one a firm can check against independent records, which is the floor a regulator expects before any account goes live.

KYC onboarding therefore comes before the moment a customer is fully onboarded or a deal closes with an individual or their organisation, because any firm that transacts first and then verifies afterward has already accepted onto its books the very risk that the screening was supposed to catch and turn away. Order is the whole point here. Until identity has been verified and authenticated, the relationship waits.

Step-by-Step KYC Onboarding Process

Sequence counts here as much as substance. Each stage of the KYC onboarding process feeds the one after it, and a shortcut taken early tends to reappear later as a gap in the audit trail. The stages run as follows:

- Introduction: First contact establishes what the customer needs and points them toward the right product or service.

- KYC Documents: The customer completes an application for an account or service and supplies the particulars a firm needs to identify them.

- Verification of Identity: A firm runs identity verification, usually checking a government-issued ID against independent data sources and asking for supporting documents. Guidance from the UK's Financial Conduct Authority (FCA) expects identity to be confirmed using government-issued documents cross-checked against trusted, independent records, which for digital-first firms translates into automated document checks and biometric facial comparison.

- Finalization: The firm completes account setup, hands over account details, and shows the customer how to use the account.

- Introduction and Follow-up: The firm welcomes the customer formally and keeps the relationship alive through continuing engagement.

Benefits of the KYC Onboarding Process

KYC onboarding protects the firm and its account holders together, because it removes risk and friction at the same time. Either party is then far less likely to be pulled into financial fraud. Catching a problem while the application is still open spares both sides the cost and delay of a remedial review that arrives long after the money has moved and the damage is already done. Prevention costs less.

A few advantages deserve naming:

- Regulatory compliance: A working onboarding programme shows that a firm applied genuine due diligence and met identity-verification standards, among them those set by AML compliance regimes.

- Market research: The documentation KYC produces lets a firm read its market with more precision, especially once it reconciles applicant PII against a digital footprint.

- Streamlining operations: Security concerns surface early through KYC, before they grow into the kind of mess that disorganised onboarding tends to breed.

- Reputational benefits: Visible verification, applied early, signals to prospective customers that a firm guards its own safety and theirs.

Put together, KYC onboarding secures compliance while it sharpens operations and raises the overall customer experience. Survey data supports this. Fenergo's 2025 survey of senior executives found that 70 percent of financial institutions lost clients over the prior year because onboarding ran too slowly, up from 67 percent in 2024 and 48 percent in 2023, and the same firms now spend an average of $72.9m a year on AML and KYC operations.

Documents Required for Customer Onboarding Process

Specific documents underpin identity verification and regulatory compliance during Know Your Customer onboarding.

Standard KYC onboarding documents include:

- A government-issued photo ID (a passport or driver's licence, for example)

- Proof of address (a utility bill or a lease agreement)

- A Social Security Number (for customers in the United States)

KYC onboarding and its relation to AML

Onboarding decisions stand or fall on how well a firm grasps its KYC and AML obligations as one body of work, since the data gathered at signup is precisely what later transaction monitoring and suspicious-activity reporting rely on to flag genuine risk. Box-ticking misses what matters. Customer confidence is earned at this stage or quietly forfeited.

- Understanding KYC/AML: Know Your Customer and Anti-Money Laundering rules are tightly braided together. Meeting both is the precondition for an onboarding process that survives scrutiny.

- Streamlined Verification: Build steady routines for identity verification, document authentication, and risk scoring, ones a firm applies case after case in place of improvising each time.

- Ongoing Monitoring: Keep customer profiles current and watch transactions as regulation shifts. United States banks gained some welcome room here in 2026. On 13 February 2026, FinCEN issued an exceptive relief order allowing covered institutions to verify beneficial owners on a relationship basis in place of doing so at every new account opening, with re-verification triggered by the first account, by facts that cast doubt on existing information, or by a firm's own risk-based procedures.

How KYC Hub Can Help Streamline KYC Onboarding Process?

Purpose-built onboarding software such as KYC Hub lets a firm compress this work and capture the upside, converting a string of manual checks into an automated flow that still produces the evidence a regulator expects to see. The gains show up across several fronts.

- Effective Customer Onboarding: Customers move through the whole journey online, which suits them and keeps the firm quick.

- Cost Saving: Shifting the process online tends to cut staffing and operational expense by a substantial margin.

- More efficient process: Digital onboarding removes friction and lowers the stress built into manual checks, and that tends to produce happier, more loyal customers.

- Better Customer Experience: A smooth, low-effort journey raises satisfaction and feeds long-term loyalty.

- Data Control: Electronic processes centralise customer data and keep it secure in a single place.

- Enhanced security: Digital onboarding adds stronger protections, among them multi-factor authentication and encryption, to shield sensitive customer data.

- 24/7 Accessibility: Customers can begin whenever and wherever suits them, which widens a firm's reach by a considerable degree.

Conclusion

Digital technology has remade the KYC onboarding process. Firms that deploy these tools shorten the time it takes to bring on a new customer, deliver a noticeably better experience, and run leaner while doing it, all the while producing the audit trail an examiner will eventually ask to see. Numbers settle most of the argument. Customers at the front and the back office behind them both come out ahead.

Firms that adopt digital onboarding solutions like KYC Hub pull clear of slower rivals while raising customer satisfaction, and the efficiency they win opens room to grow.