Know Your Customer (KYC): What It Is, Process, and Compliance

Know Your Customer (KYC) is the compliance process that financial institutions use to verify the identity of their customers, understand the nature of their activity, and assess the risk that a relationship may be used for money laundering or other financial crime. It pulls identity verification, customer due diligence, and ongoing monitoring into a single control framework. For banks, fintechs, and other regulated firms, KYC is both a legal obligation and the bedrock of an effective anti-money laundering program.

The stakes are high. According to the United Nations, money laundering costs up to $2 trillion every year. And a 2025 Fenergo study found that 70% of financial institutions lost clients in the past year because of slow, inefficient onboarding, which is exactly why so many compliance teams are moving toward digital KYC verification. This guide explains what KYC means for regulated businesses, how the process works, the documents and components involved, and the regulations that govern it.

What Is Know Your Customer (KYC)?

Know Your Customer (KYC) is the set of procedures a regulated business follows to confirm that a customer is who they claim to be and to gauge the risk that customer presents. Firms collect identifying information, verify it against reliable sources, and review the customer's activity over the life of the relationship. The goal is simple: prevent fraud, money laundering, and terrorist financing while keeping the institution compliant with applicable regulations.

The full form of KYC is "Know Your Customer." In casual use the term gets reduced to a single onboarding check, but for a compliance team it means an ongoing program rather than a one-time event. Tie onboarding, risk assessment, and continuous review together, and the institution always holds a current, accurate picture of who it is dealing with.

What Is the Full Form of KYC?

The full form of KYC is Know Your Customer. In regulated financial services it is sometimes extended to "Know Your Customer and Customer Due Diligence" to reflect that identity verification and risk assessment are part of the same obligation.

Objectives of KYC

The main objective of KYC is to verify customer identities and prevent money laundering and financial fraud. For a B2B compliance team, the four primary objectives are:

- Customer identification: confirm the customer is a real, identifiable person or entity.

- Risk management: each customer gets a risk profile, with controls sized to match.

- Regulatory compliance: meet the obligations regulators set, and prove that compliance when examiners ask.

- Trust and integrity: shield the institution, and the wider financial system, from abuse.

KYC has been around for decades, yet it carries more weight now that transactions have grown more complex and more cross-border. Tighter regulation pushes firms to take real measures to know their customers, and anti-money laundering controls sit directly on top of the KYC framework. AML procedures monitor transactions, flag suspicious activity, and report incidents to authorities. None of that works without the customer knowledge KYC produces.

Overview of the KYC Process

The KYC process can be broken down into several stages that run from onboarding through the entire relationship:

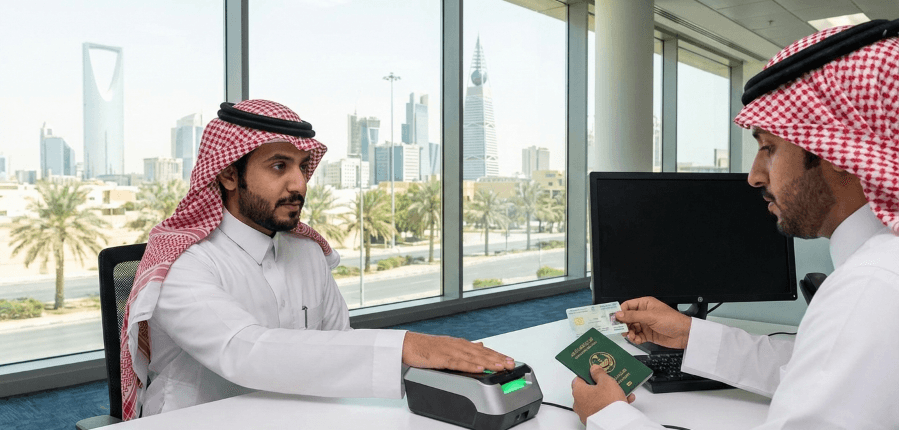

- Customer onboarding: When a new customer wants to open a relationship, the institution collects and verifies identifying information before the account goes live.

- Customer Identification Program (CIP): Basic details get gathered here, such as name, date of birth, and address, then checked against documents or trusted data sources.

- Customer Due Diligence (CDD): This stage digs deeper. It captures source of funds and the intended nature of the relationship so the institution can assess risk.

- Ongoing monitoring: Institutions keep watching customer transactions and activities to confirm behavior matches the expected profile and to catch shifts in risk.

- Reporting and recordkeeping: Records of identification, risk assessments, and transaction monitoring are kept on file, and suspicious activity gets reported to the relevant authorities.

What Are the Stages and Components of KYC?

Compliance teams usually describe KYC in terms of three core components and four operational stages. The three components are the Customer Identification Program, Customer Due Diligence, and Ongoing Monitoring. Add risk management as a distinct discipline and you get the four stages:

- Customer Identification Program (CIP): Obtain and verify identifying information such as name, address, date of birth, and supporting documents.

- Customer Due Diligence (CDD): A risk assessment determines how much risk a customer poses and whether enhanced due diligence is warranted.

- Ongoing monitoring: Customer information is reviewed and updated on a regular basis, with risk levels reassessed as circumstances change.

- Risk management: Match controls to risk, train staff, and keep the program governed and documented.

Fold anti-money laundering measures into these stages and ongoing monitoring gets sharper. Where KYC and AML work in step, compliance holds up better and the control environment becomes more transparent and easier to defend.

KYC Documents Meaning: What Documents Does KYC Require?

KYC documents are the evidence a customer provides so an institution can verify identity and assess risk. The exact set depends on the industry, the jurisdiction, and whether the customer is an individual or a business. Common categories include:

- Government-issued ID such as a passport or driver's license.

- Proof of address, which can be a utility bill or a recent bank statement.

- Tax identification or national identity number.

- For businesses, registration documents such as a certificate of incorporation or business license, plus information on beneficial owners.

Together these documents establish identity and let the institution screen the customer against watchlists and sanctions lists. With corporate customers, collection goes further, reaching the ultimate beneficial owners and the ownership structure behind the entity.

Know Your Customer Compliance and Regulations

Know Your Customer compliance means meeting the legal obligations that require regulated firms to identify customers, assess risk, and monitor activity. Fall short and the consequences are steep: substantial fines, sanctions, even the loss of an operating license. Regulations vary by country but share one purpose, protecting the integrity of the financial system. Key frameworks include:

- Financial Action Task Force (FATF): Sets the global standard for KYC and AML measures through its recommendations.

- Bank Secrecy Act (BSA): The primary US legislation governing KYC and AML, requiring a Customer Identification Program and reporting of suspicious transactions to FinCEN.

- USA PATRIOT Act: Enacted after 2001, this law widened customer identification and verification obligations for US financial institutions.

- EU Anti-Money Laundering Directives: A series of directives setting KYC and AML requirements across the European Union.

Verifying customers before opening a business relationship started in the 1970s in the United States, written into the Bank Secrecy Act to combat money laundering. Requirements then shifted sharply after the September 11th attacks in 2001 and again following the 2008 financial crisis. Today, KYC compliance is non-negotiable for anyone operating in the global financial system. Knowing these standards well helps firms dodge penalties and harden their defenses against financial crime at the same time.

What Is KYC Verification and What Affects Its Reliability?

KYC verification is the act of confirming that the identity information a customer provides is genuine and accurate. The IFC has noted that strong KYC verification can improve customer due diligence in smaller or more difficult emerging markets. When verification is inaccurate or incomplete, criminals can exploit financial institutions to launder money or commit fraud, and the firm absorbs the legal, financial, and reputational fallout.

Several factors determine how reliable KYC verification turns out to be in practice:

- Data accuracy and completeness: Bad or missing data leads to flawed identity decisions, so accuracy at onboarding is everything.

- Quality of data sources: Verification is only as good as the sources behind it. They need to be authoritative and current.

- Verification processes and procedures: Well-defined procedures, reviewed regularly, keep decisions consistent across the team.

- Staff training and expertise: Trained people make better calls and keep pace with regulatory change.

Firms that want to improve reliability set clear policies, lean on trusted data sources and verification tools, keep customer data current, and invest in ongoing training. Modern KYC verification software handles much of this automatically, which cuts human error and keeps the process consistent and auditable.

The Role of Technology in KYC

Manual KYC struggles to keep pace as regulatory expectations climb. Technology lifts both the accuracy and the speed of verification by automating data collection, document verification, and risk assessment. Capabilities compliance teams reach for include:

- Digital identity verification: Remote, real-time identity checks using facial recognition, biometrics, and electronic document verification.

- AI and machine learning: Models comb through large volumes of data and surface suspicious patterns a human reviewer might miss.

- Regulatory technology (RegTech): Tools that automate the KYC process end to end, from identification through reporting.

Automate the repetitive checks and you cut the time and cost of KYC, sharpen consistency, and leave a clear audit trail. That hits the pain points compliance teams know best: onboarding delays, high false-positive rates, and the grind of keeping records current across jurisdictions.

Anti-Money Laundering and Know Your Customer: How They Connect

KYC and AML are closely linked, but they are not the same thing. KYC is the customer-facing discipline of knowing who you are dealing with. AML is the broader program of detecting and preventing money laundering, and it covers transaction monitoring, suspicious activity reporting, and risk assessment. KYC feeds AML directly. No institution can monitor transactions well or judge whether activity is suspicious without first knowing the customer behind the account.

In practice, the two run as one continuous control loop. Onboarding sets identity and a baseline risk rating, ongoing monitoring watches for deviations, and anything anomalous feeds back into the customer's risk profile. Run KYC and AML as a single connected program and a compliance function can scale without giving up coverage.

Challenges in Implementing KYC at Scale

KYC is essential, but building and running an effective program is hard, especially for firms operating across borders. Common challenges include:

- Cost and complexity: KYC takes real resources to stand up and maintain, which can stretch a smaller compliance team thin.

- Data privacy and security: Collecting and storing customer data brings privacy obligations and exposure to cyber risk.

- Customer experience: Heavy onboarding frustrates customers and drives up drop-off, so firms have to balance rigor against friction.

- Global requirements: A globalized financial system means working through different KYC regulations across jurisdictions, each with its own rules and documentation standards.

The firms that handle these pressures best treat KYC as one unified, technology-driven program rather than a pile of disconnected manual checks.

How KYC Hub Helps: Global KYC Solution for Banks and Fintechs

KYC Hub offers a Global KYC Solution built for banks and fintechs that need to onboard customers fast while staying fully compliant. The platform brings together the core pillars compliance teams rely on: video KYC, identity verification, document-based ID verification, digital signature, liveness check, and phone verification. All of it runs through a single onboarding and verification flow, so teams verify identity, confirm documents, and capture consent without stitching together a handful of point tools.

Built for global operations, the solution supports the document standards and verification methods that jurisdictions require, with continuous monitoring layered on top to keep risk profiles current. You get faster onboarding, fewer manual reviews, and an auditable record that holds up to regulatory scrutiny. To see how the Global KYC Solution fits your onboarding and compliance workflow, get a free demo.