Customisable Screening & Monitoring Process

KYC Hub’s AML Screening and Monitoring solution screens for better accuracy, allowing contextual and fuzzy matching, entity resolution, aliases and associations. With our Screening and Monitoring solution, you can onboard customers with ease without having to worry about violating sanctions. Our intuitive screening process and AML checks tracks global sanction lists and adverse media to give you accurate and timely risk assessment.

Best in Class AML Screening & Monitoring Designed To Help You Scale Up

Exhaustive AML Screening

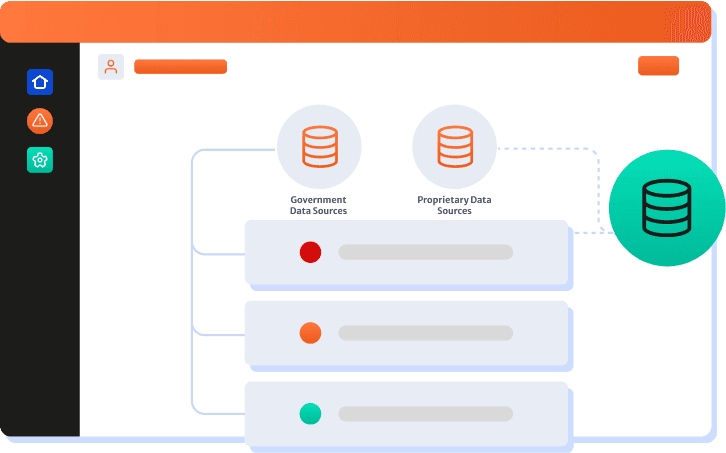

Our solution helps you comply with regulations by identifying individuals and entities on various watchlists. You can now automate AML screening and monitoring against live real-time data. Get access to up-to-date datasets and 1000s of sanction lists across 200+ countries. Better fraud detection through daily updates and continuous monitoring.

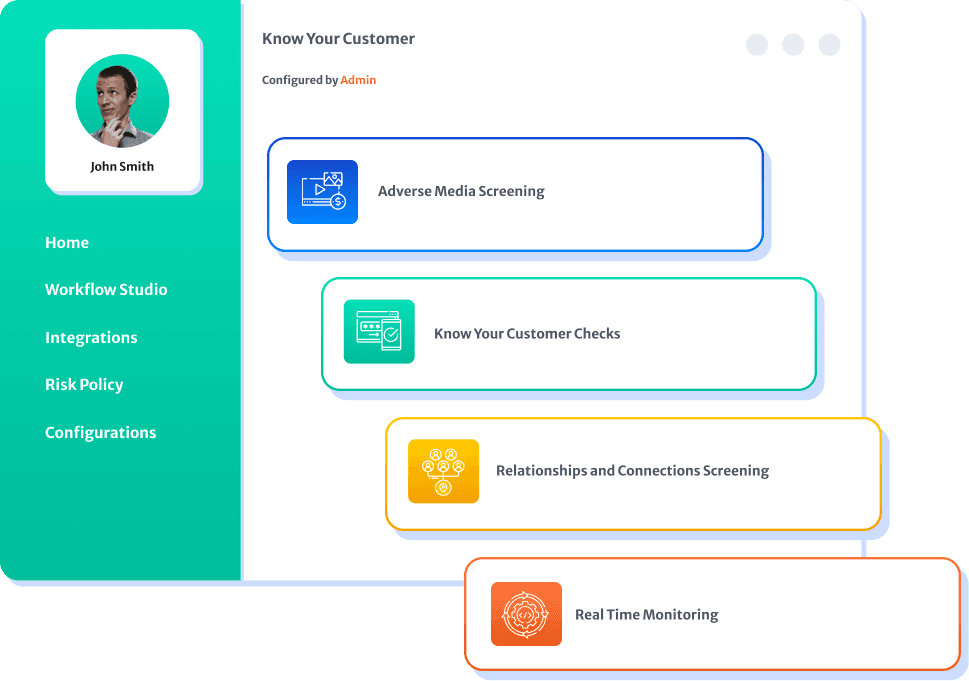

Authenticate Your Customers & Partners With Ease

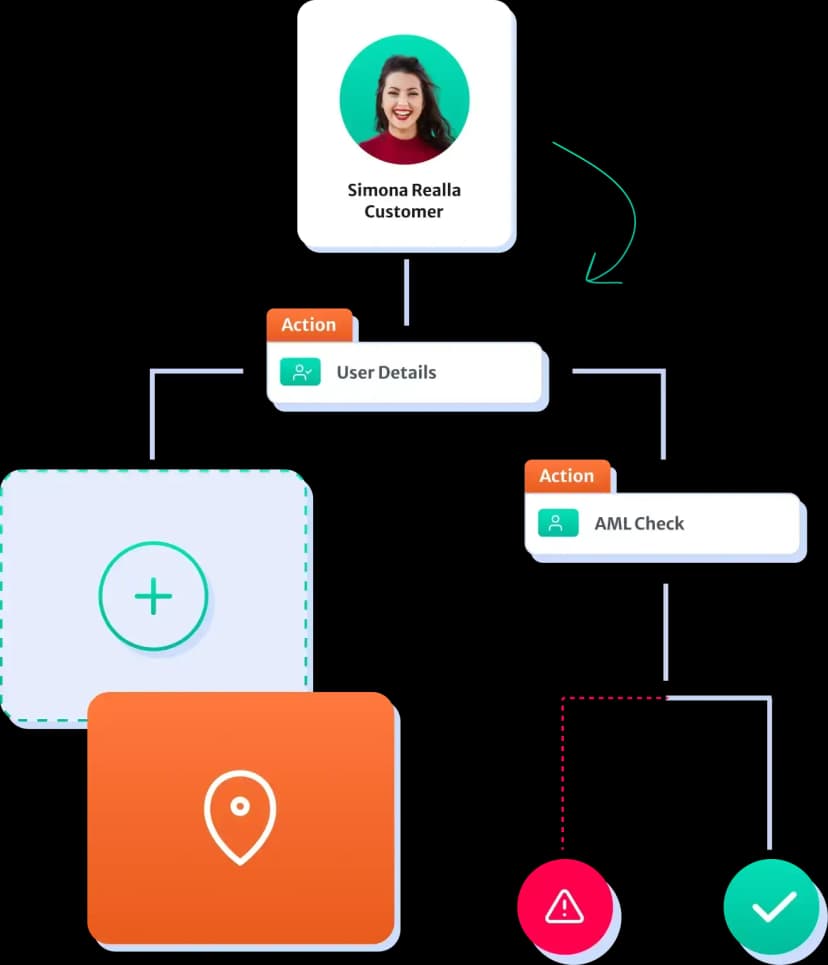

Build your own Customer Due Diligence (CDD) program with KYC Hub. Screen their identity documents, check against sanction lists, Politically Exposed Persons (PEPs), and other dynamic global lists. Set up a custom onboarding process for your customers and ensure that you are safeguarded against money laundering.

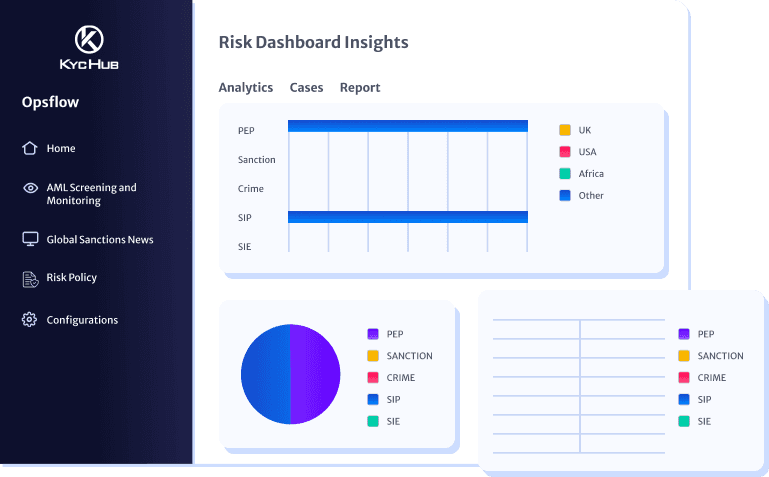

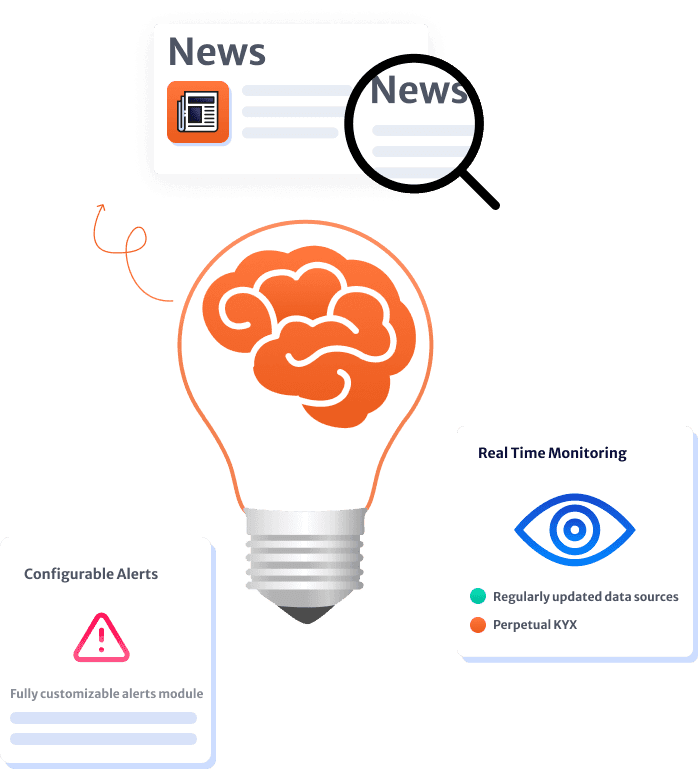

Continuous Monitoring & AML Alerts

Receive instant notification alerting you about changes to the risk status of the entities you monitor with actionable insights to avoid non-compliance. Using our state-of-the-art risk-based due diligence approach, you will be alerted of changes in a customer's risk profile in real-time so that you can take proactive action.

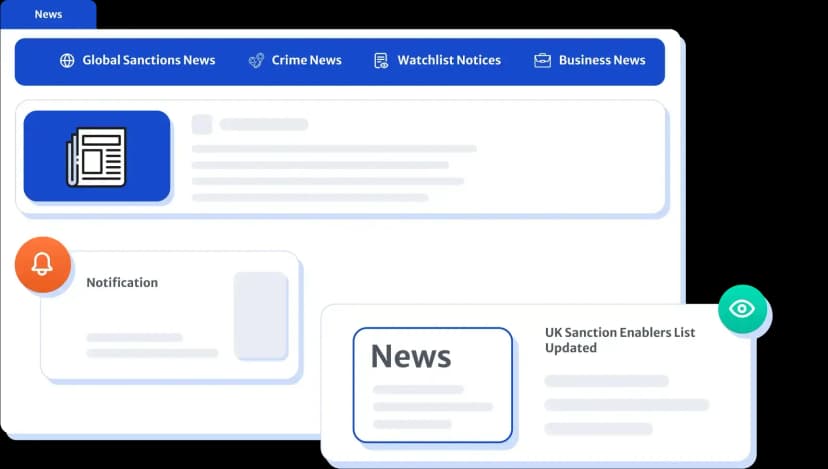

Global Adverse Media Intelligence

A sophisticated and advanced media intelligence system to help you track and monitor adverse news about individual and corporate clients , while suggesting specific topics to follow. Screen against sanctions, PEPs, and global watchlists. Leverage our proprietary contextual matching and entity resolution algorithms to only receive relevant alerts and avoid false positives.

Screening for Watchlists, Sanctions, and PEPs with AML Checks

AML checks can help you to keep up with anti-money laundering checks and have enhanced due diligence measures for spotting financial crimes or illegally obtained funds. KYC Hub assists you in following money laundering regulations and keeping an eye on global AML watchlists, sanctions list, and PEPs.

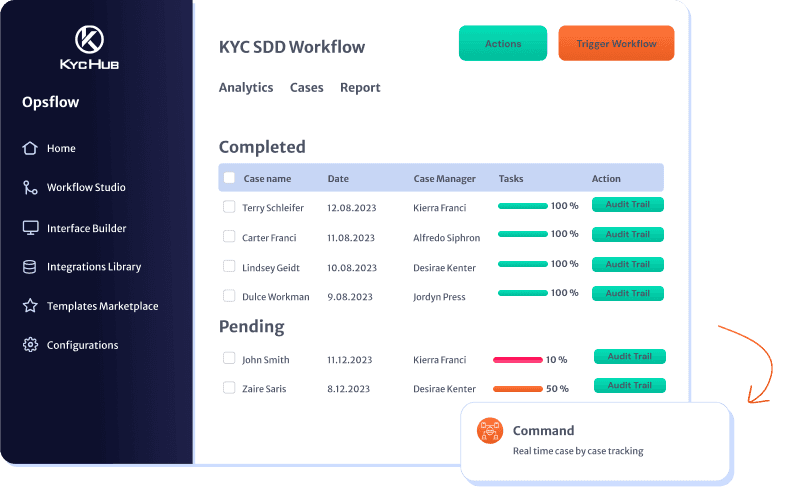

Increase Operational Efficiency and Stay Compliant and Secure Always

Automated screening processes designed to help you save time and scale faster. Simple API integrations to optimize turnaround time. Reviews are faster than ever with intelligent monitoring to reduce false positives and minimize costs and efforts. KYC Hub helps you focus on security and compliance and safeguarding your company against bad actors and ever-changing regulations.

Why Customers Vouch For KYC Hub’s AML Screening Solution?

Advanced Network Analysis Algorithms That Detect Connections & Risks

Network Intelligence

Advanced Network Analysis Algorithms That Detect Connections & Risks

Global Data Coverage

Expansive Access To Global Data Sources and Continuously Updated Data

Fewer False Positives

Reduction in False Positives With Via State of The Art Matching Algorithm

Operational Efficiency

Automated Processes That Drive Operational Efficiency

Easy Integration

Seamless Integration with Multiple Modes for Easy Implementation

Risk-Based Due Diligence

Efficient customer risk assessment to facilitate Risk Based Due Diligence Approach

[ RELATED ]

Explore Our Other Products and Use Cases

Discover more about our products and solutions. Explore the rest of the KYC Hub stack.

Any questions? We got you.

Discover more about our products and solutions. Embark on your journey towards seamless compliance.