Identity Verification Methods: A Guide for Compliance Teams

Identity verification methods are the techniques a business uses to confirm that a customer is who they claim to be before granting access to an account, a product, or a transaction. Some check a government-issued document. Others match a live selfie against that document, query authoritative databases, or pose knowledge-based questions. Picking the right mix is the foundation of a defensible KYC program for any regulated firm, and a core control against fraud and financial crime.

No single method wins every use case. Compliance teams weigh assurance level against fraud resistance, onboarding friction, cost, and how well a method covers different customer segments. That balance is rarely obvious. Below we go through the main identity verification methods, explain how each one works, and show where each fits inside an AML and KYC framework.

What is Identity Verification?

Identity verification is the process of proving that a person is who they claim to be using official, independently sourced evidence rather than self-asserted information. In a compliance context it underpins Customer Identification and the broader Know Your Customer obligation. A firm has to establish and record a customer's identity before onboarding, then keep that assurance current over the life of the relationship.

For AML-regulated businesses, none of this is optional. Strong verification supports fraud prevention, protects sensitive customer data, and demonstrates compliance with Anti-Money Laundering (AML) and Know Your Customer (KYC) requirements. Methods range from basic document examination all the way to high-assurance biometric recognition. Most mature programs combine several.

Why Identity Verification Methods Matter for Regulated Firms

For banks, payment firms, fintechs, and other obliged entities, the verification method you choose carries direct compliance and commercial consequences. Banks and financial institutions have to verify identity before opening an account. Done well, that stops identity theft and money laundering at the point of entry. The same checks then support authorisation of high-value transactions and protect legitimate account owners' access to their funds.

Lenders verify identities for a slightly different reason. They need to confirm an applicant is real before assessing creditworthiness, and to cut down on fraudulent applications. Across all of these activities, strong identity verification is what lets a firm actually comply with AML and KYC regulations instead of treating them as a box-ticking exercise. The methods below differ sharply in how well they meet each of these goals.

Identity Verification Methods Compared

What follows are the most widely used identity verification methods, each with its own strengths and limitations for a compliance program.

Document-Based Verification

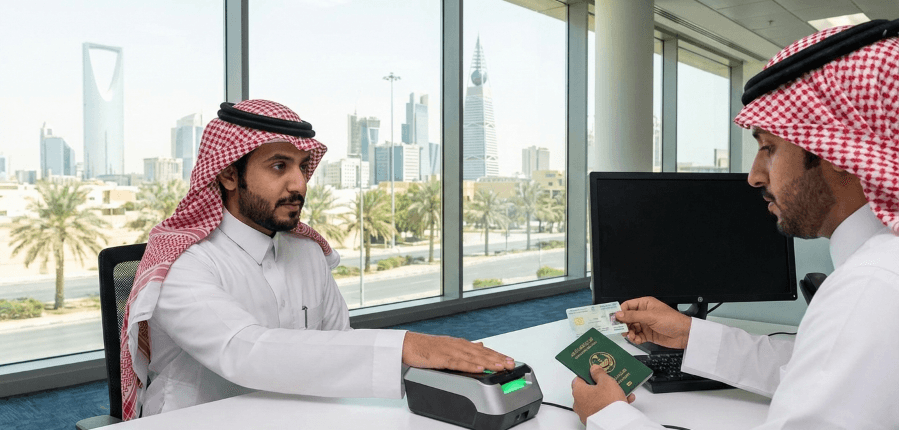

Document verification checks the authenticity of government-issued IDs to confirm identity. Think passports, driver's licenses, and national ID cards. It reads the security elements, checks that the data on the document is internally consistent, and lifts the text out with optical character recognition (OCR).

A typical flow runs in four steps. First, the user captures or uploads their ID. OCR extracts the text and data from the document. Authenticity checks then inspect security features such as holograms and watermarks for any sign of tampering or forgery. As a final step, the extracted data is cross-referenced against the information the user provided and against database records.

Document verification produces highly reliable evidence, and it works well for remote onboarding and digital transactions. That is exactly why banking, e-commerce, and government bodies rely on it. There are trade-offs, though. A well-made counterfeit ID can sometimes slip past basic checks, and a blurry scan slows everything down and may force a manual review. Even the simple effort of locating and submitting a document can drag down onboarding completion rates.

Biometric Authentication

Biometric authentication uses physical or behavioural characteristics to verify a person, things like fingerprints, facial recognition, voice patterns, and iris scans. Unique biological traits are extremely hard to counterfeit or duplicate, which is what makes biometric authentication strong. Financial services, healthcare, and law enforcement all rely on it.

Common biometric methods include:

- Fingerprint recognition, which scans and matches fingerprints for authentication.

- Facial recognition analyses a person's features and compares them to a stored or document image. It is now the default for remote onboarding.

- Iris scanning: the unique patterns in a person's iris.

- Voice recognition, identifying individuals by their vocal patterns.

The big draw is high assurance with very little user effort. Customers never have to remember a password or PIN. Data privacy and security are the flip side. Biometric data has to be protected to an exceptionally high standard, because once it leaks you cannot reissue it the way you would a password. Capture also needs special hardware or a compatible device, and accuracy can slip in poor lighting or where a fingerprint has been affected by injury or a skin condition.

Database Verification

Database verification compares user-supplied information against authoritative databases. The submitted details are usually name, address, and date of birth, checked against government records, utility records, and financial institutions. The goal is to confirm that the data lines up with a legitimate, independently held source.

Three stages, in practice. The user submits core personal details, the system queries a set of approved databases, and the identity clears once those records line up with what was submitted. Because it leans on established records, database verification asks little of the user and keeps onboarding fast and low-friction.

Automation and scale are its real strengths. Large volumes of customers can be verified without manual effort, which suits high-throughput banking and e-commerce operations. The limitations are real, though. A check is only as good as the accuracy and freshness of the data behind it, so stale or incomplete records mean failed checks and frustrated customers. Coverage thins out, too, for groups with little record history, such as young adults or residents of underbanked areas, and the method demands strong data protection controls.

Credit Bureau-Based Authentication

Credit bureau-based authentication verifies personal records against credit bureau databases. The records checked include a Social Security number and address history, drawn from Equifax, Experian, and TransUnion. Financial services firms use it heavily to confirm identity, and in lending it doubles up to assess credit standing at the same time.

A user provides personal details, the system checks them against credit bureau records, and the identity is confirmed if the details match. Credit files hold a large volume of financial history, so fabricating a consistent record is genuinely difficult for a fraudster. For monetary transactions and loan approvals, that makes it a high-assurance method.

Its main limitation mirrors database verification. People without a credit history, including new immigrants and young adults, struggle to pass, and that raises a financial-inclusion concern. Results also hinge entirely on the accuracy of bureau data. And because it involves sharing sensitive financial information, it carries a heavy data protection burden.

Knowledge-Based Verification (KBV)

Knowledge-based verification (KBV) asks an individual personal questions whose answers come from their credit history and public records. Take "What was your previous address?" or "Which bank holds your mortgage?" The system pulls questions from credit bureau and public-record data, the user picks an answer from several options, and each response is checked back against the source records.

Deployment is easy. KBV needs no special hardware and no biometric capture, and it returns a result quickly. Many firms run it as a supplementary layer alongside other methods.

For compliance use, the weaknesses are significant. So much personal data has leaked in breaches that an attacker may already hold the answers, which means KBV should never be a standalone control. Customers with thin or outdated records also struggle to answer correctly. Worse, security questions can be guessed or pulled out of someone through phishing.

Multi-Factor and Two-Factor Authentication (2FA)

Two-factor authentication (2FA) requires a user to present two distinct factors before gaining access. Typically that is something they know, like a password or PIN, paired with something they have, like a one-time code sent by SMS, email, or an authenticator app. Even when an attacker cracks one factor, the second one makes unauthorised access far harder to pull off.

It holds up well against credential-stuffing and password-only breaches, which is why it has become a standard control for account access and step-up verification. Its limitations are operational rather than fundamental. Lose the registered device or app and a user can be locked out. SMS codes carry their own risk: they are vulnerable to SIM-swap attacks, and one-time passwords can be phished. For high-risk actions, 2FA works best paired with stronger methods rather than used alone.

One point is easy to miss. No single method should carry an entire program. A layered approach gives the best balance of assurance and customer experience, with document and biometric checks at onboarding, then database screening and step-up authentication for risky events.

Book an Identity Verification Demo

Identity Verification Requirements in a KYC Program

Choosing methods is only part of the picture. Regulated firms have to map each method to a documented requirement: who needs to be verified, to what assurance level, and how the evidence is retained for audit. Under a risk-based approach, a low-risk retail customer might clear with a document and database check, while a higher-risk relationship calls for biometric matching and enhanced due diligence.

Verification is also not a one-time event. Records age, risk profiles shift, and a name that was clean at onboarding may later surface on a watchlist. Mature programs treat verification as continuous, refreshing identity assurance and re-screening customers over the life of the relationship rather than only at account opening.

How KYC Hub Approaches Identity Verification

KYC Hub provides identity verification for global customers built around the controls compliance teams actually need. The platform leads with facial biometrics and a liveness check that confirms a real, present person rather than a photo or a replay, then matches that capture against the customer's identity document for high-assurance onboarding.

Stronger verification should not come at the cost of completion rates. So the flow stays quick and low-friction, pairing document, biometric, and database checks in one place. Comprehensive reporting hands auditors a clear evidence trail for every decision. For high-risk transactions, enhanced security lets firms add step-up checks wherever the risk warrants it. AI and machine learning back each stage, so teams verify customers faster without giving up a defensible compliance record.